China’s onshore corporate bond market – understanding recent market volatility

27/11/2020

China’s bond market has seen an unusual wave of defaults over the past month – triggering a jump in credit spreads and raising investor concerns. Aidan Shevlin, Head of Asia Pacific Liquidity Management, and Andy Chang, Credit Analyst, relate the implications to cash investments and explain why independent credit research remains important.

Q1. What were the major recent events that generated the RMB corporate bond market volatility?

There were three major defaults (listed below) and several other credit events where perpetual bonds were not called or bond coupons were not paid. In 2020, the pace of RMB corporate bond defaults has been unusually low, so the recent flurry of defaults caused investor uncertainty.

There were three major defaults (listed below) and several other credit events where perpetual bonds were not called or bond coupons were not paid. In 2020, the pace of RMB corporate bond defaults has been unusually low, so the recent flurry of defaults caused investor uncertainty.

Q2. What does the issuers’ rating mean and what are their implications to money market funds (MMFs)?

While some of these issuers are rated AAA by onshore rating agencies, they do not have international ratings. Despite domestic and international rating agencies using the same rating scale, domestic rating agencies typically place considerable weight on the implicit presence of government support for bond issuers and rely less on organizations’ financial data. It is possible that some locally rated MMF owned their securities, however these securities would not be approved by institutional MMFs with AAA international rating – which have much stricter guidelines.

Q3. Has the pace of Chinese onshore defaults increased?

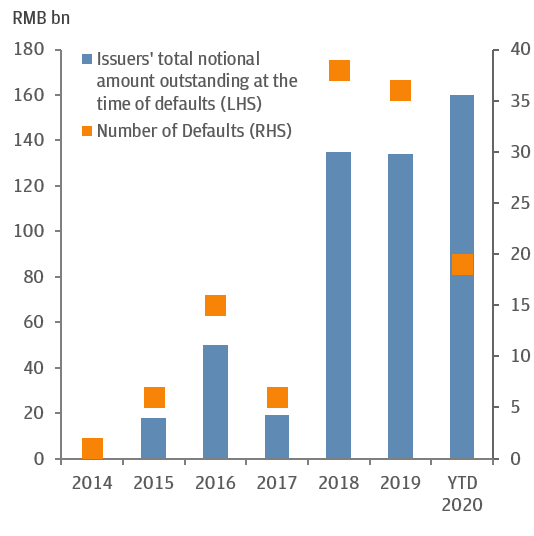

Since the first bond default in 2014, the number and size of Chinese onshore defaults has increased each year (Fig 1). Having said that, Chinese onshore defaults remain relatively low by international standards, with 36 defaults totaling approximately RMB 130bn in 2019.

Strong government support, lower interest rates and plentiful liquidity in the first half of 2020 reduced the pace of defaults as the government sought to stabilize the economy following the Covid-19 pandemic. However, with the pandemic contained, market interest rates have normalized while government support has faded. This increased the challenges for highly indebted corporate bond issuers to pay coupons and issue new debt.

FIGURE 1: CHINA ONSHORE BOND DEFAULTS

Q4. What was the trigger for the current market volatility?

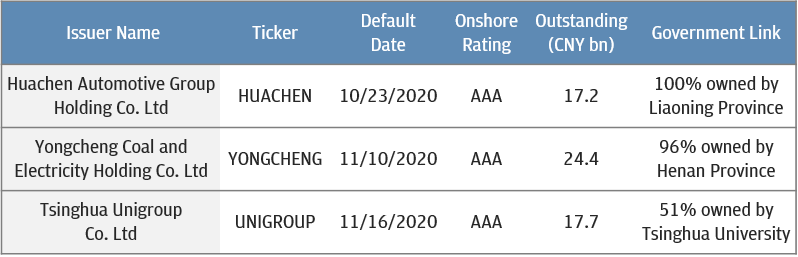

Early in November, Yongcheung Coal and Electricity Holding Co. Ltd, a state owned enterprise (SOE) rated AAA by Chinese domestic rating agencies, defaulted on CNY 152m of bonds. Within the following few weeks, several other high profile borrowers also defaulted while at least 20 corporate bond issuers suspended plans to issue new debt.

Historically, onshore rating agencies and investors assumed that state linked companies benefitted from an implicit government guarantee. Regardless of weak financials, SOE issuers were widely considered immune to credit volatility. However, state owned does not mean state guaranteed. The recent defaults have shaken investor confidence and increased scrutiny of other SOE issuers with weak profitability and high levels of borrowing.

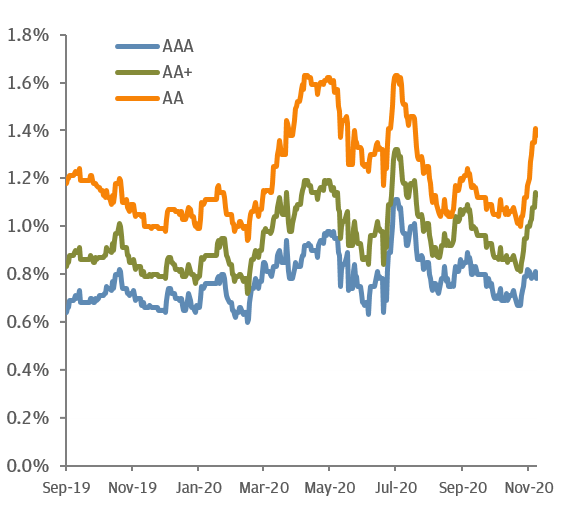

Onshore credit market spreads have widened sharply (Fig 2), especially for issuers in similar industries or with similar levels of government support. Meanwhile, the price of corporate bonds issued by the companies in default have fallen steeply.

FIGURE 2: 3-YEAR CORPORATE BOND SPREADS RELATIVE TO 3-YEAR GOVERNMENT BOND YIELDS

Q5. What steps have the government taken to calm market sentiment?

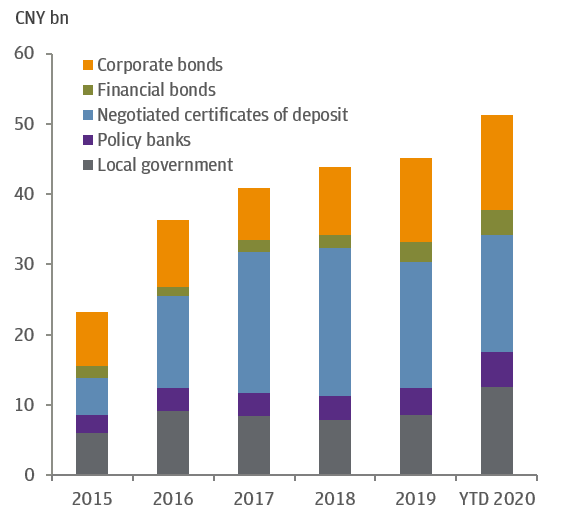

Given the size and importance of the onshore corporate bond market (Fig 3), the authorities are keen to minimize market turbulence. The Financial Stability and Development Commission of the State Council met on the 21st of November to investigate recent bond market developments and ensure its stability.

The meeting called for adopting a "zero-tolerance" stance, safeguarding the fairness and order of the market, strictly investigating and penalizing illegal and non-compliance activities (such as fraudulent issuance, false disclosure of information, malicious transfer of assets and misappropriation of issuance proceeds), severely punishing acts of liability evasion, and protecting investors’ legitimate rights and interests.

Meanwhile, the People’s Bank of China (PBoC) continued to inject funds via open market operations to ensure adequate market liquidity. The combined actions boosted bond market confidence, and bond prices declined subsequently.

FIGURE 3: CHINESE BOND MARKET'S ANNUAL ISSUANCE

Q6. What is the outlook for the onshore corporate bond market?

The government, PBoC and regulators are keen to strengthen the link between risk and return, while reducing the perception of implicit government guarantees. They are also focused on reducing the size of the shadow banking market and minimizing systemic risks.

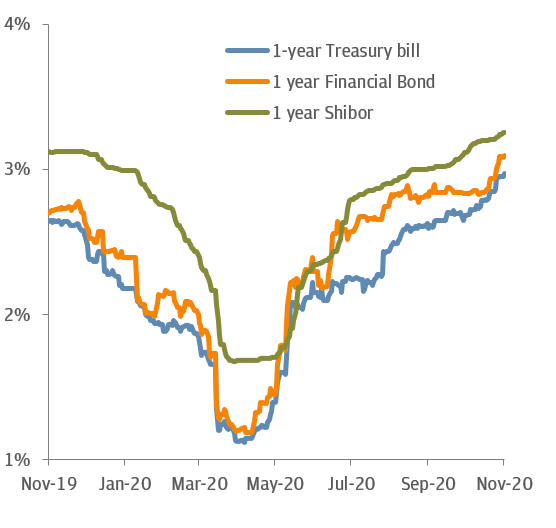

Therefore, it is likely that the pace of bond defaults will return to more normal levels over the coming months, as government support fades and interest rates remain relatively high (Fig 4). The type of defaults will likely broaden beyond private companies as government support for SOEs fades.

FIGURE 4: SHORT-TERM YIELDS IN CHINA

Q7. What are the implications for cash investors?

Given the limited benefit of onshore credit ratings, these defaults re-emphasizes the importance of high quality in-house credit research. Rigorous analysis of issuers and counterparties is critical to understanding the true underlying risk characteristics of onshore credit investments.

A robust investment policy, combined with independent credit research and an objective analysis of the potential level of government support of issuers, are critical steps that can minimize downside risks whilst allowing cash investors to take advantage of the evolving market opportunity.