Week in review

- China GDP grew 4.3% y/y in 2Q26

- U.S. inflation increased 3.5% y/y in June

- China exports increased 27% y/y in June

Week ahead

- China 1Y loan prime rate

- Korea 2Q26 GDP growth

- Japan June inflation rate

Thought of the week

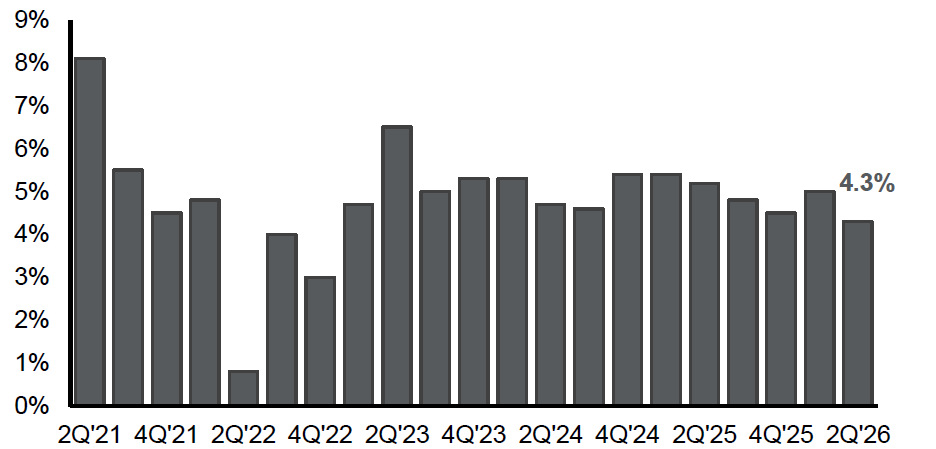

China’s 2Q26 GDP miss highlighted a recovery that remains within target but is losing momentum. Growth slowed to 4.3% year over year, while first-half growth of 4.7% stayed inside the official range. The divide remains clear: exports, advanced manufacturing, and technology-linked supply chains are supporting activity, while weak consumption, contracting investment, and persistent property stress continue to drag on domestic demand. Industrial profits have improved, but not enough to signal a broad reflation cycle. The data should increase expectations for a more supportive policy tone, though likely through targeted measures rather than large-scale stimulus. The key is whether policy can broaden demand beyond export-led and high-tech sectors, while market leadership may remain tied to structural upgrading and global competitiveness.

China real GDP

Year-over-year change

Source: FactSet, National Bureau of Statistics China, J.P. Morgan Asset Management. Data reflect most recently available as of 16/07/2026.

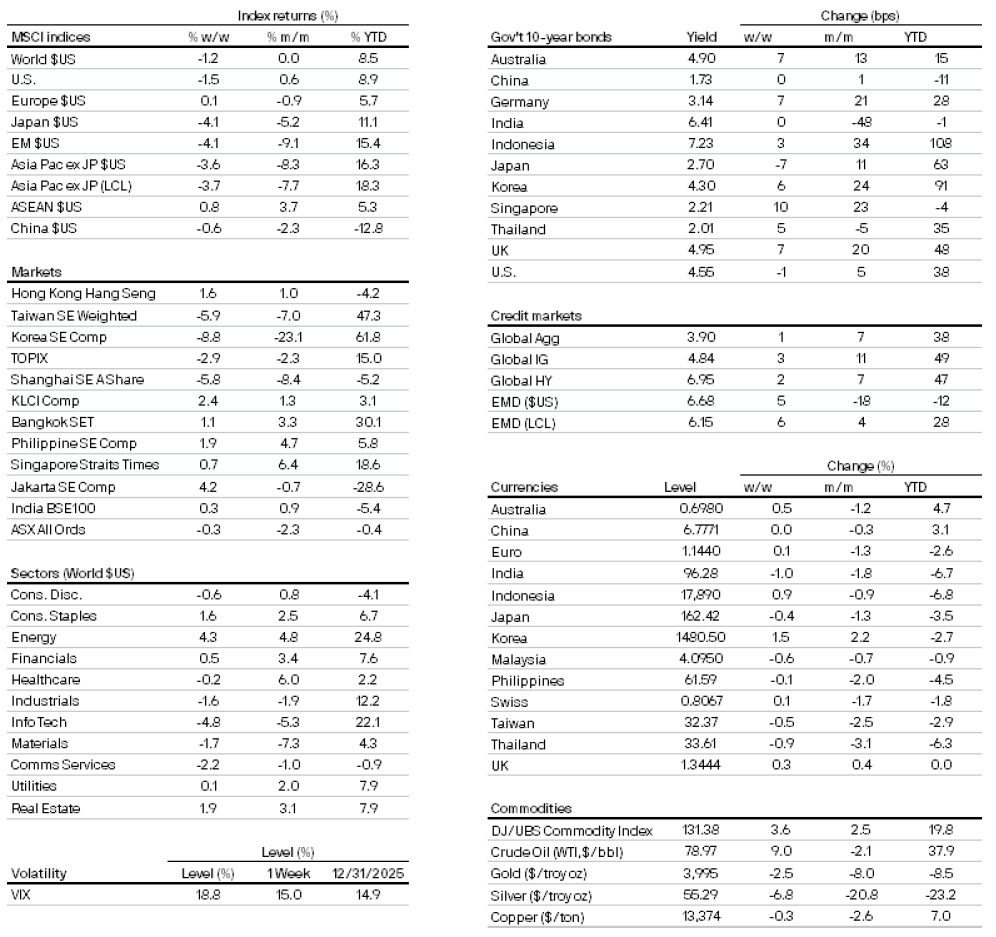

Market data

300a4900-f9d9-11e8-839f-fe2ee17e7f12

All returns in local currency unless stated otherwise.

Currencies’ return are based on foreign currencies per U.S. dollar. An appreciation of the foreign currency against the U.S. dollar would be positive and a depreciation of the foreign currency against the U.S. dollar would be negative.