What do our Long-Term Capital Market Assumptions mean for DC plans?

14-07-2023

Emily Cao

Annabel Tonry

Our 2023 Long-Term Capital Market Assumptions, which forecast asset class returns over a 10- to 15-year horizon, suggest that public markets today offer the best potential long-term returns in more than a decade. For those who are early in their retirement savings journey, this is unequivocally good news. For their older colleagues, however, the situation may not be so rosy – after all, forecasts of higher returns tomorrow are simply the flip side of recent capital losses.

Examining these two perspectives can be a “teachable moment,” shedding light on what makes up a successful outcome for defined contribution (DC) members.

A much-improved long-term outlook

From today’s vantage point, the outlook for future returns is much brighter than it has been in many years. A year ago, high valuations for stocks and bonds reduced our long-term return assumptions to their lowest levels in decades. Then came the bear market of 2022, in which stocks and bonds both suffered significant losses – a rare phenomenon. Amid the heightened level of market volatility and the absence of diversification across traditional asset allocations, we made two key observations.

First, the ability of active managers to diversify portfolios away from the concentrated exposures of capitalisation-weighted passive benchmarks may have delivered differentiated performance. And second, alternative asset classes, such as real estate, provided a measure of risk reduction as they shielded capital from the simultaneous stock and bond downturn.

Our forecasted annual return for a 60/40 stock-bond portfolio has jumped to 7.20%

Exhibit 1: Annual 60/40 Portfolio Return Projections, 2010–2023

Source: J.P. Morgan Asset Management Long-Term Capital Market Assumptions. Forecasts are not a reliable indicator of future results.

The outlook has since been transformed. Following the past year’s market decline, our forecasted annual return for a 60/40 stock-bond portfolio over the next 10 years has almost doubled, from 4.30% last year to 7.20% (Exhibit 1).

A fully invested portfolio will benefit from a market recovery, but, of course, such a portfolio has recently experienced losses that will need to be recovered. Contributions invested today would be expected to generate materially higher long-term returns, accelerating the portfolio’s recovery and augmenting its long-term performance.

The three lessons for DC members

The defined contribution system is designed to foster the patient accumulation of capital over a working lifetime and then to put that capital to use in delivering adequate income during retirement. Given the long time horizons involved, one might be tempted to assume that timing and luck don’t matter much – that it all averages out in the end.

While this may well be true for younger members, it does not apply to savers later in their working lives. DC members can find themselves subject to a great deal of timing risk if their portfolio experiences a severe market drawdown as they approach or enter retirement, leaving them with insufficient assets for adequate income replacement and little time to recover their losses.

Market risk is inescapable. But trustees and members can take actions to mitigate its effects. A thoughtful and disciplined investment strategy, implemented via a well-designed DC plan utilising industry best practices can go a long way towards setting members up for a successful retirement. Therefore, while members make critical decisions within their own DC plans, trustees can do a great deal to set up members for a positive outcome.

There is no simple roadmap, however. The challenges posed by the current environment will serve to test existing models and suggest enhancements for the future. As markets transition through a period of exceptional volatility, three key lessons are worth remembering:

Fortitude is needed to remain invested during periods of market volatility and to maximise contributions to the extent possible.

Foresight is required to reduce risk patiently and carefully as retirement approaches, avoiding market risk at the most critical moments.

Flexibility is essential during the transition from accumulation to decumulation, when the need for income replaces the need for total return.

Fortitude: Investing through downturns to achieve long-term goals

There is an oft-repeated adage that “success is not about timing the market, it’s about time in the market.” Broadly speaking, this is excellent advice. Staying the course and remaining invested through the market’s ups and downs is a proven approach to capital accumulation. In some periods, valuations are high and contributions earn lower returns. At other times, valuations are lower and contributions earn much higher returns. Investors, even those later in their working lives, should be wary of pulling money out of the market in response to short-term negative returns.

History suggests that timing the market correctly is very difficult, even for savvy professional investors. For DC plan members, the odds are long indeed. Often, risk aversion rises after a market sell-off, leading investors to de-risk too late. Conversely, markets often rebound strongly from their lows, and capital that has sought the safety of low risk asset classes can miss out on the much-needed upside. Fortitude is needed to stay invested, to stay diversified and to maintain contributions over time.

What does all this mean at the granular level of DC plan allocation and investment? A disciplined asset allocation strategy that embraces prudent risk-taking and diversification across market sectors has the potential to deliver long-term returns with acceptable risk. As we are wise to remember that although diversification does not eliminate the risk of loss and as market conditions change, the use of active management within default strategies can allow a member’s portfolio to respond to market shifts by proactively deviating from market benchmarks while remaining fully invested. Finally, maintaining contributions during periods of volatility ensures that members won’t miss attractive entry points.

Foresight: De-risking as retirement approaches protects members

Whatever the phase in the market cycle, an individual member makes a critical choice in deciding when to retire. Someone who experiences a significant market downturn immediately before or after retiring may suffer long-term financial consequences. The loss of capital may diminish a member’s ability to earn sufficient income in retirement. To earn back losses, a member may need to take on additional risk. Both of these situations are clearly undesirable.

Fortunately, though, steps can be taken to help protect a member from the fallout of a “retirement eve” bear market. In practice, the main action is to reduce market risk in the period leading up to retirement. It is far better to forgo some potential returns in the last few years of a working life than to risk the disaster of a downturn striking at exactly the wrong moment.

A well-designed default strategy aims to accomplish this goal by reducing asset risk as the strategy matures and members approach retirement. Including lower volatility active fixed income strategies can mitigate the effects of sudden market moves. Allocations to alternatives can also be of benefit, providing diversification from public markets.

Flexibility: Finding retirement income and risk diversification

As members transition from working life to retirement, their portfolios must undergo two shifts from capital accumulation: first to capital preservation and then to income generation. Flexibility is essential, as the markets will determine how much income is available and where it comes from. Income might be the yield on diversified fixed income securities and/or the dividend payments from equity and certain alternative strategies.

US Aggregate Bond Index yields have risen sharply over the past year

Exhibit 2: US Aggregate Yields, November 2021–November 2022

Source: Bloomberg, J.P. Morgan Asset Management; data as of 10 November 2022.

The bond market today offers much higher levels of yield than at any time in the past decade (Exhibit 2). DC savers who are already in retirement have a compelling opportunity to lock in high levels of income. For workers nearing retirement, who may have lost a portion of their capital in the recent sell-off, the higher yields are a welcome relief. Equity strategies with an income focus may also offer attractive dividend yields, as well as the opportunity to participate in any future market rebound.

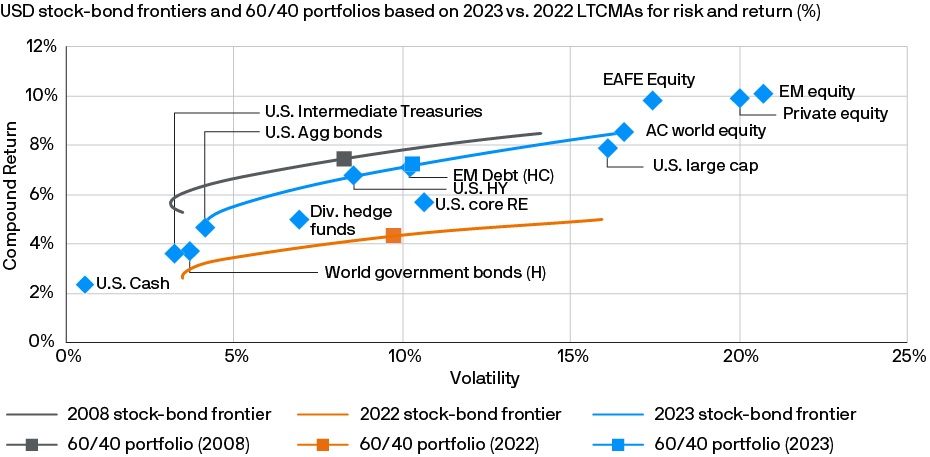

As our 2023 Long-Term Capital Market Assumptions analysis illustrates, stock-bond frontiers rose significantly over 2022, with much improved returns now expected for bonds, equities and alternatives. Of particular note is the plot for alternative asset classes, which thrives to offer the potential for alpha, inflation tapering, and diversification (Exhibit 3).

Exhibit 3: USD Stock-Bond Frontiers and 60/40 Portfolios Based on 2023 Vs. 2022 Long-Term Capital Market Assumptions for Risk and Return (%)

Source: J.P. Morgan Asset Management; data as of September 30, 2022.

In the current market environment, providing access to diversified sources of returns for DC members will be critical. As such, a default fund that offers a diversified allocation across fixed income sectors, equities and alternatives may be well positioned, particularly when augmented by active management – including both bottom-up security selection within individual strategies and flexible top-down asset allocation, allowing positioning to shift as opportunities change across time.

Luck is not a strategy

Today’s investing environment is testing DC strategies. For trustees, it will be critical to establish a plan design that facilitates continuing investments over time, offers prudent risk reduction as retirement approaches and delivers income in retirement.

Successful retirement planning is built around long-term averages, not short-term extremes. Yet in volatile markets, some DC savers, feeling whipsawed between good and bad fortune, may look to reduce or even stop contributions. To keep members on track, trustees will need a well-designed default strategy that can turn volatility into an opportunity through diversified investments and prudent risk management. Three virtues – fortitude, foresight and flexibility – can guide members and trustees in the direction of a successful retirement outcome.

09vw230307154658