In Brief

- The Bank of England (BoE) raised the Bank Rate by 50 basis points (bps) to 2.25% in a split 5-3-1 vote as the tight labour market, higher wages and higher domestic inflation justified a seventh consecutive hike.

- With a technical recession now forecast for the UK in the third quarter, the government’s Growth Plan should serve to support household spending and reduce the peak in near-term inflation. However, stronger demand could add to medium-term inflationary pressures and ultimately lead to higher rates.

- Even as ultra-low yields become a distant memory, short-term investors should stay alert. Policy is “not on a pre-set path”, and combined with increased geopolitical risk, a weaker currency and the start of active quantitative tightening (QT), interest rate volatility is likely to continue.

Divided opinion

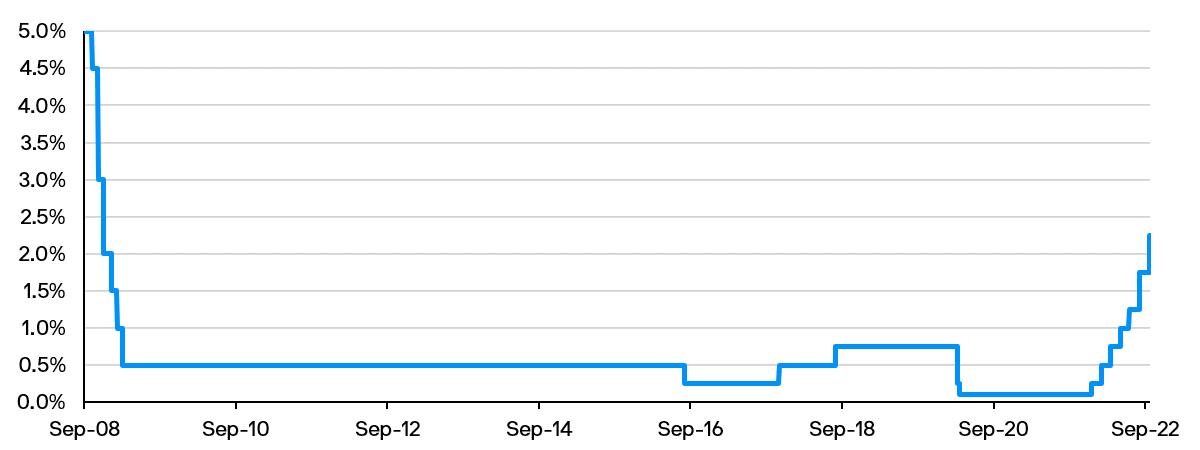

Ahead of the September Monetary Policy Committee (MPC) meeting – which had been delayed one week by the death of Queen Elizabeth II –market uncertainty regarding the potential future pace of BoE rate hikes was elevated. Ultimately, the Monetary Policy Committee (MPC) retained their August cadence, and raised the Bank Rate by 50bps to 2.25%, the highest level since November 2008 (Exhibit 1).

Exhibit 1: UK bank rate at 2.25% for first time in nearly 14 years

Source: Bank of England, data as at 22 September 2022.

Source: Bank of England, data as at 22 September 2022.

Notably, the decision was split three ways – highlighting the complex economic challenges facing the central bank. Five MPC members voted in favour of a 50bps hike, three members judged that an immediate 75bps hike would guard against the “risks of a more extended and costly tightening cycle later”, while the newest MPC member, Swati Dhingra, dissented with a vote to raise rates more slowly by 25bps. Concurrently, the MPC unanimously agreed to reduce the stock of UK government bonds held within the Asset Purchase Facility by £80 billion over the next year, through both maturing Gilts and active QT Gilt sales.

Technical recession ahead of a fiscal boost

Second quarter 2022 GDP fell 0.1%, better than the BoE had expected given the extra bank holiday for the Queen’s jubilee celebration. However, with third quarter GDP now forecast by the BoE to contract 0.1%, the UK will likely record a technical recession of two consecutive quarters of negative growth, as weaker manufacturing and construction, an additional bank holiday for the Queen’s funeral, and the continued squeeze on real disposable incomes further weigh on economic activity.

Material upside inflation pressures remain

With consumer spending estimated by BoE agents to have peaked in the third quarter, a boost in demand should come from the government’s Energy Price Guarantee, which will cap household energy bills for two years, and provide equivalent support for businesses over six-months. The scheme means that consumer price index (CPI) inflation is now expected to peak sooner, and by less, reaching just under 11% in October 2022.

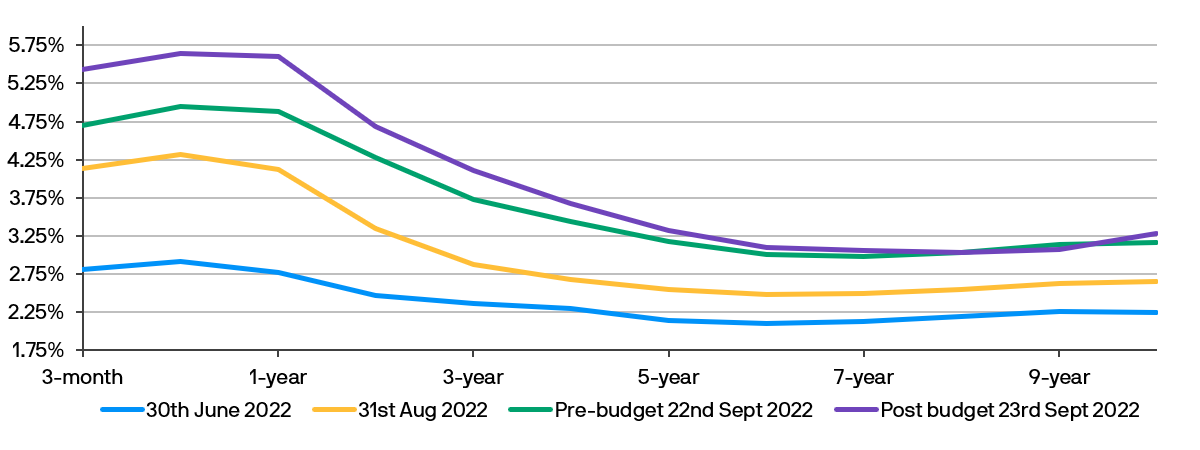

While the Energy Price Guarantee should protect against externally generated price inflation in the near term; it could also lead to less constrained household spending. Alongside continued tightness in the labour market and a more recent rapid increase in nominal wages (which have risen despite a surprising jump in inactivity and some indications of weakening demand for labour), these domestic cost pressures may serve to increase inflation and inflationary expectations in the medium term. Furthermore, the tax cuts and additional fiscal measures announced in the government’s Growth Plan on Friday 23 September have also fuelled expectations of higher inflation. The BoE did make clear that the fiscal support package would be material for the economic outlook and that the MPC will make a full assessment of the impacts at its November meeting. However the massive fiscal support measures have significantly heightened monetary policy uncertainty regarding the future cadence of rate rises and the ultimate terminal Bank Rate (Exhibit 2).

Exhibit 2: UK SONIA forward curves are now projecting a higher terminal rate

Source: Bloomberg, data as of 23 September 2022. SONIA - Sterling overnight index average rate. Exhibit shows expected forward SONIA rates 1 year ahead.

Investor implications

Sterling cash investors should welcome this further increase in the Bank Rate, with improved overnight rates allowing liquidity and ultra-short duration strategies to boost returns – albeit with a slight delay due to the need to wait for the reinvestment of maturities. However, the BoE was keen to stress that the pace of interest rate rises is not on a pre-set pace and the MPC would respond forcefully, as necessary.

A number of factors, including ongoing geopolitical concerns, the weakness of sterling, increased government borrowing and active quantitative tightening are all expected to add to the volatility for UK interest rates. Therefore, we recommend sterling investors maintain a disciplined approach to cash segmentation, and prioritising a combination of money market and ultra-short duration strategies, which should ensure they can to optimise returns without excessively increasing risk or volatility.

09oy222609140940

For Professional Clients/ Qualified Investors only – not for Retail use or distribution.

This is a marketing communication and as such the views contained herein are not to be taken as advice or a recommendation to buy or sell any investment or interest thereto. Reliance upon information in this material is at the sole discretion of the reader. Any research in this document has been obtained and may have been acted upon by J.P. Morgan Asset Management for its own purpose. The results of such research are being made available as additional information and do not necessarily reflect the views of J.P. Morgan Asset Management. Any forecasts, figures, opinions, statements of financial market trends or investment techniques and strategies expressed are, unless otherwise stated, J.P. Morgan Asset Management’s own at the date of this document. They are considered to be reliable at the time of writing, may not necessarily be all inclusive and are not guaranteed as to accuracy. They may be subject to change without reference or notification to you. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and investors may not get back the full amount invested. Past performance and yield are not a reliable indicator of current and future results. There is no guarantee that any forecast made will come to pass. J.P. Morgan Asset Management is the brand name for the asset management business of JPMorgan Chase & Co. and its affiliates worldwide. To the extent permitted by applicable law, we may record telephone calls and monitor electronic communications to comply with our legal and regulatory obligations and internal policies. Personal data will be collected, stored and processed by J.P. Morgan Asset Management in accordance with our EMEA Privacy Policy www.jpmorgan.com/emea-privacy-policy. This communication is issued in Europe (excluding UK) by JPMorgan Asset Management (Europe) S.à r.l., 6 route de Trèves, L-2633 Senningerberg, Grand Duchy of Luxembourg, R.C.S. Luxembourg B27900, corporate capital EUR 10.000.000. This communication is issued in the UK by JPMorgan Asset Management (UK) Limited, which is authorised and regulated by the Financial Conduct Authority. Registered in England No. 01161446. Registered address: 25 Bank Street, Canary Wharf, London E14 5JP.