In brief

- The RBA’s cumulative 300bps increase in base rates across eight meetings since May marks its longest consecutive period of rate hikes ever. However, monetary policy typically operates with a lag and the RBA noted that the full effect of the increase in interest rates is yet to be felt in mortgage payments.

- With the 25bps not fully priced in, the AUD strengthened, while, bond yields were slightly higher across the curve. Hawkish comments encouraged markets continue to price in two additional rate hikes in 2023, with a terminal rate of 3.60% by mid-year.

- The lack of a monetary policy meeting in January will allow the RBA time to assess the impact of the recent, consecutive rate hikes. Nevertheless, with inflation remains uncomfortably high – a number of additional rate hikes are likely before a longer pause is advisable.

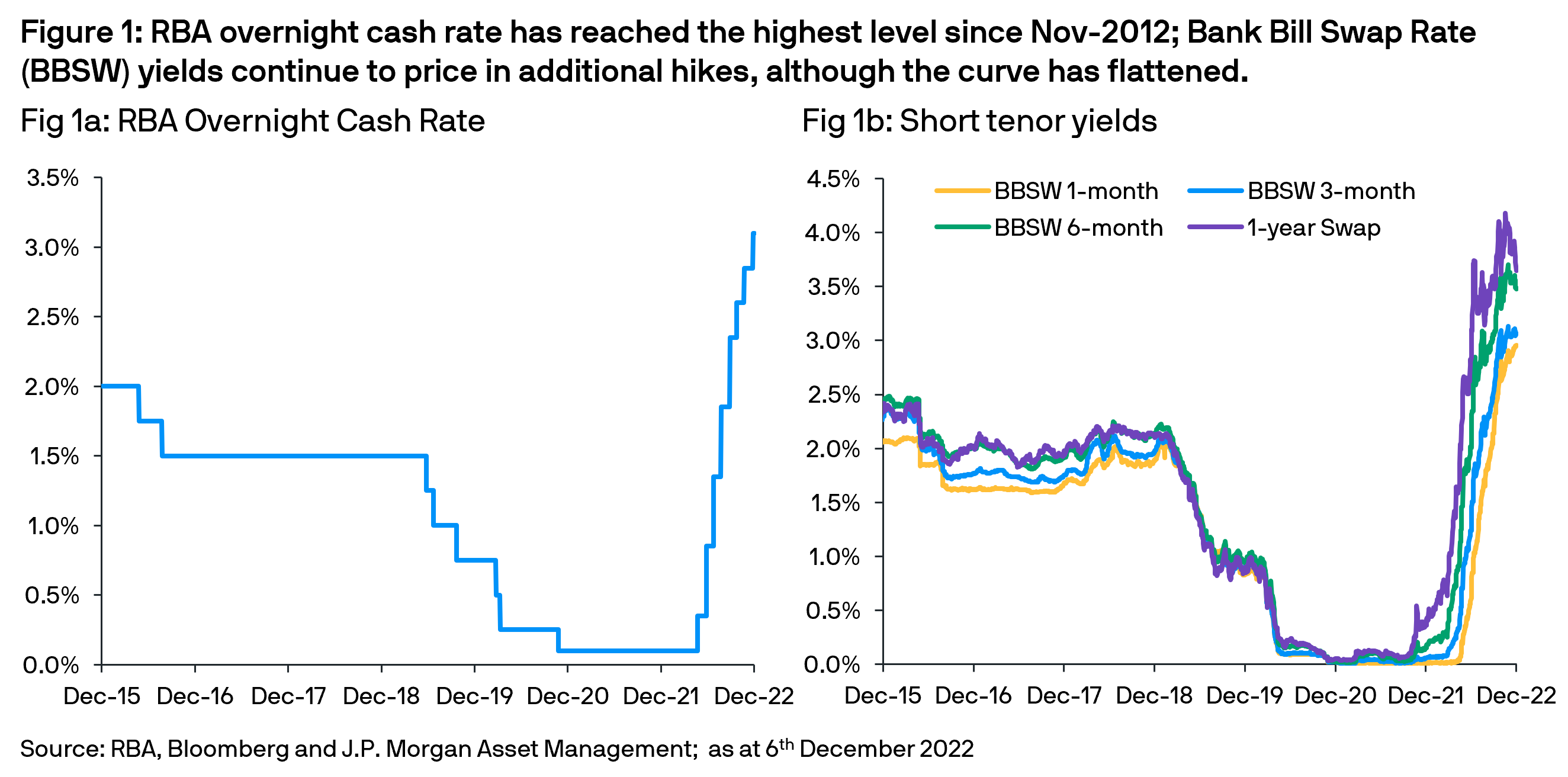

At their final monetary policy meeting of 2022, the Reserve Bank of Australia (RBA) raised its Overnight Cash Rate (OCR) by 25bps to 3.10%. The widely anticipated hike takes base rates to a decade high of 3.10% (Fig 1a). In the accompanying statement, the RBA continued to balance its “resolute” determination to curtail inflation, which it regards as “too high”. The central bank also noted the need to “keep the economy on an even keel”, before concluding that while further increases were likely, it was not on a pre-set course.

Consecutive hikes and policy lags:

The cumulative 300bps increase in base rates across eight meetings since the start of May represents the longest consecutive period of rate hikes ever by the RBA. Acknowledging the “substantial cumulative increase in interest rates”, the central bank noted that it “has been necessary to ensure that the current period of high inflation is only temporary” and its “priority is to … return inflation to the 2-3% range over time”.

Australian inflation remains elevated, as global factors, strong domestic demand and tight labor markets continue to elevate prices. Consequentially, wage price data also continues to trend upwards, hitting a nine-year high of 3.1%y/y (Fig 2a) in the third quarter. However, determining the future trajectory and potential peak of inflation has become more challenging as readings for the new monthly CPI series (Fig 2b) have started to deviate from the long-established quarterly CPI series (Fig 2a). The latter, released prior to the previous RBA monetary policy meeting, showed prices hitting a 48-year high of 7.3%y/y. In contrast, after hitting 7.3%y/y in September, the former slipped to a lower than expected 6.9%y/y in October.

Notably, while the RBA referenced the monthly rate in its accompanying comments, it still bases forecasts on the quarterly reading – with latest Statement on Monetary Policy report forecasting inflation peaking at 8.0%y/y in the fourth quarter. Meanwhile, the new monthly reading has several caveats, most notably, it only surveys approximately 60% of the prices contained in the quarterly series and is not yet seasonally adjusted – reducing its usefulness.

As the RBA observed, monetary policy typically operates with a lag – determined by demand for credit and how closely borrowing rates are correlated with central bank base rates. With “the full effect of the increase in interest rates yet to be felt in mortgage payments”, the RBA will likely welcome the lack of a monetary policy meeting in January. The hiatus until the next monetary policy meeting on the 7th of February 2023 will provide a natural pause, allowing the RBA to assess the impact of the recent, rapid consecutive rate hikes.

No dovish pivot yet

The RBA’s recognition that “the Australian economy is continuing to grow solidly” and that “inflation is too high”, establishes a strong rationale for future rate hikes. Indeed, the central bank confirmed that “a further increase in inflation is expected over the months ahead” and “the Board expects to increase interest rates further”.

This hawkish view combined with the latest hike not being fully priced in, triggered a strengthening of the AUD, while bond yields were slightly higher across the curve. Markets continue to price in approximately two additional rate hikes in 2023, with OCR reaching a terminal rate of 3.60% by mid-year.

Outlook:

With the RBA forecasting a decline in growth and inflation in 2023, its commitment to future hikes remains in doubt – despite its comments were more hawkish than expected – and debate has pivoted to a future pause and potential peak. Fortunately, the lack of a monetary policy meeting in January will allow the RBA time and access to several new pieces of data – including the fourth quarter inflation rate – to assess the impact of the recent, consecutive rate hikes.

Nevertheless, with inflation remaining uncomfortably high and base rates only entering restrictive territory – a number of additional rate hikes are likely necessary before a longer pause is advisable – to safeguard against the risks of a “prices-wages spiral” and ensure “inflation expectations remain well anchored”.

For AUD cash investors, the latest rate hike and confirmation that more hikes are likely is positive news. Money market and ultra-short duration strategies could present increasingly attractive current income opportunities, while providing shelter from the still volatile longer duration fixed income strategies.

This information is generic in nature provided to illustrate macro trends based on current market conditions that are subject to change from time to time. This generic information does not take into account any investor’s specific circumstances or objectives and should not be construed as offer, research or investment advice.