In brief:

- At its semi-annual monetary policy meeting on 14 October, the MAS re-centered the mid-point of the S$NEER up to its prevailing level while keeping the slope and width of the policy band unchanged.

- The MAS forecasts headline and core inflation will remain above their historical averages for some time. It also believes Singapore will grow at a pace that is below trend in 2023.

- Immediately following the MAS announcement, Singapore bond yields declined while the currency softened. Elevated inflation had raised expectations that the MAS would enact a more hawkish dual tightening, but balancing inflation and growth concerns potentially deterred more aggressive MAS policy actions.

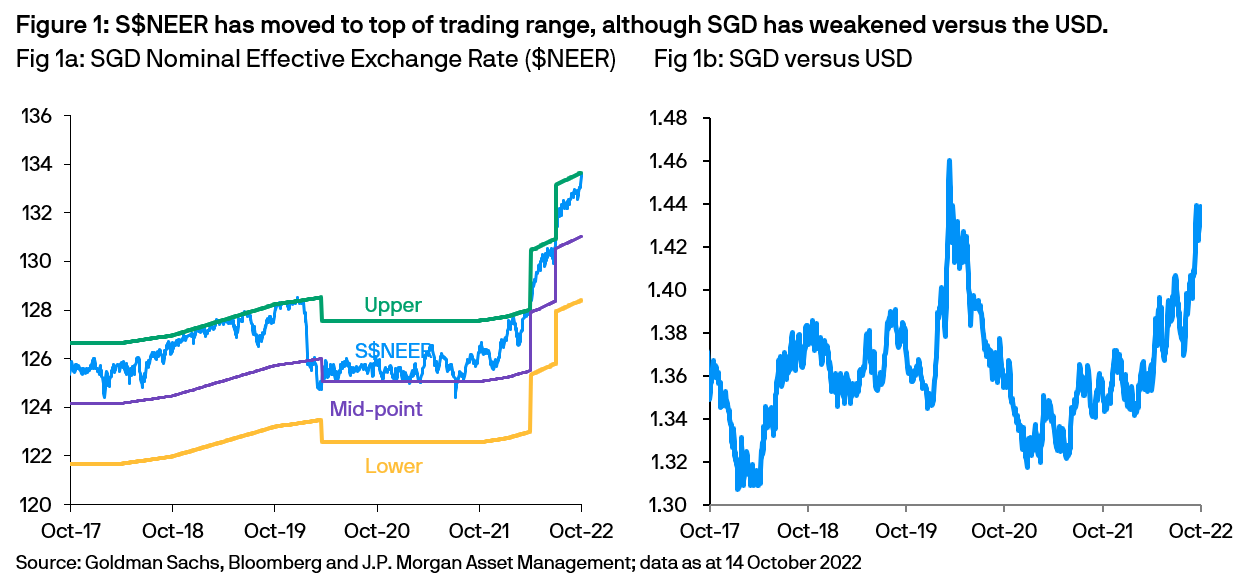

At its semi-annual monetary policy meeting on 14 October, the Monetary Authority of Singapore (MAS) re-centered the mid-point of the S$NEER (Fig 1a) up to its prevailing level – approximately a 2% increase – while keeping the slope and width of the policy band unchanged. This was the fifth hawkish monetary policy action by the MAS, as a rebound in third quarter growth allowed it to “lean against price pressures becoming more persistent”. Notably, while the central bank observed that cost pressures would linger and inflation risks remain to the upside, it also expects GDP to moderate next year, which potentially deterred more aggressive MAS policy actions.

Elevated inflation yet slower growth

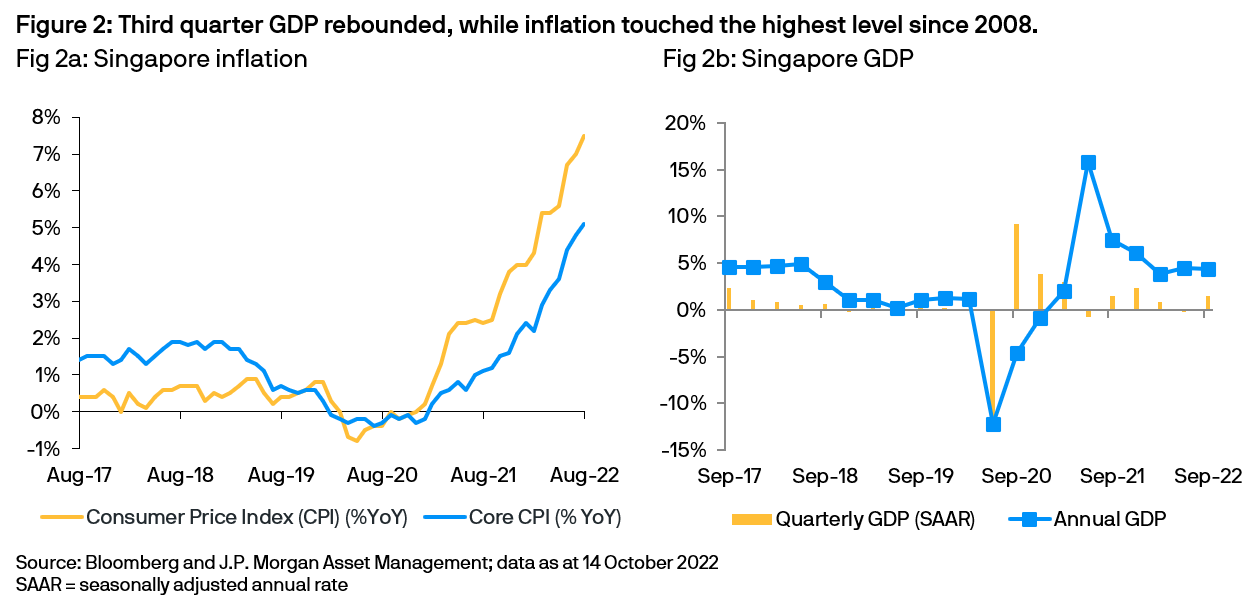

Headline inflation hit a 14-year high of 7.8%y/y in August on broad based price pressures, while core inflation jumped to 5.1%y/y (Fig 2a). Despite an early and significant hawkish policy pivot by the MAS in 2021 and “globally synchronized tightening in monetary policy” this year, the central bank believes “core inflation will stay elevated over the next few quarters as imported inflation remains significant and a tight labor market supports strong wage increases”. It forecasts 2022 headline and core inflation will average 6% and 4% respectively before easing to 5.5-6.5% and 3.5-4.5% in 2023 as cost pressures ease and commodity prices moderate. The MAS acknowledged these levels are still above historic averages, and there is still “upside risks to these forecasts” due to unexpected shocks and second round effects.

Concurrently, advanced third quarter GDP (Fig 2b) rebounded by a faster than expected rate at 1.5%q/q as stronger domestic and tourist demand helped offset manufacturing and financial services weaknesses. This allowed the MAS to reaffirm its full year 2022 growth forecast of 3-4%. Nevertheless, with “prospects for Singapore’s manufacturing sector and some trade-related services… dimmed” and the pace of domestic spending likely to “moderate... with sentiment softening”, the central bank believes “Singapore’s GDP will come in below trend in 2023”.

Market reaction

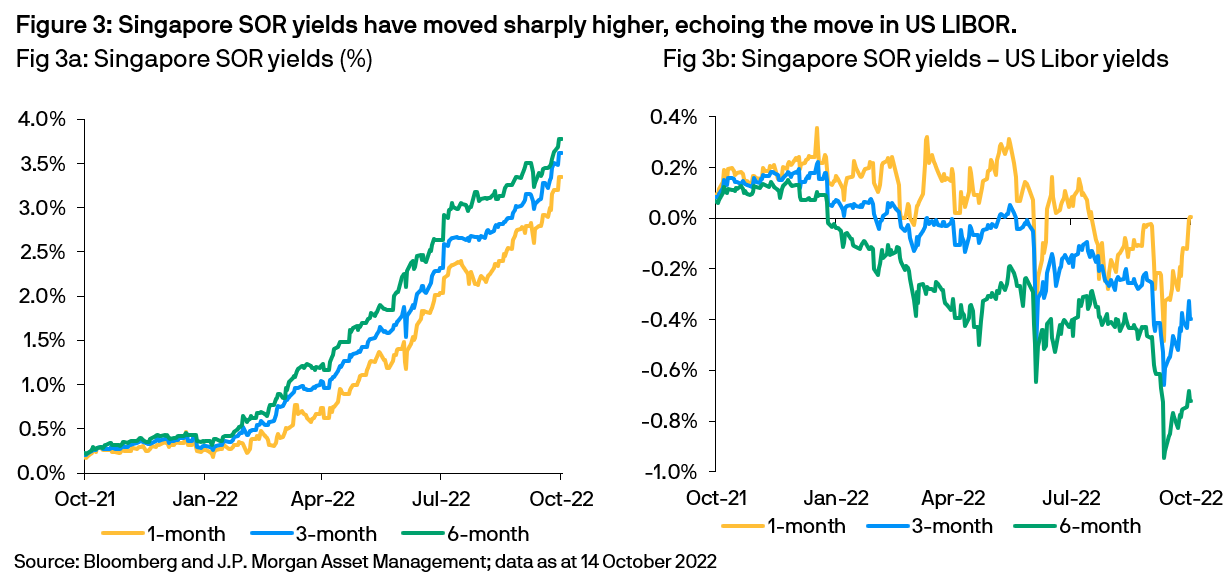

Immediately following the MAS announcement, Singapore SOR (Fig 3a) and bond yields declined while the currency (Fig 1b) softened. Elevated inflation had raised expectations that the MAS would enact a more hawkish dual tightening – adjusting the slope and re-centering the S$NEER. However, this type of more aggressive action has only occurred twice in the last two decades – in April 2020 as the pandemic hit global markets and in April 2022 as the current inflation challenge became more apparent. While increasing the slope helps moderate price trends over a longer period of time, we believe a re-centering is a more appropriate response to the immediate inflation concerns – especially against the backdrop of “imported inflation … across a range of intermediate and final goods”.

Outlook

The MAS believes its hawkish actions will “help dampen inflation in the near term and ensure medium term price stability, providing the basis for sustainable economic growth”. Nonetheless, given its position as an open, trade-dependent economy, external factors including global and regional growth, international inflation trends and the Federal Reserve’s monetary policy will continue to have a significant impact on domestic outcomes.

Over recent months, Singapore’s short-tenor yields have continued to climb higher (Fig 3b), a welcome result for SGD cash investors. Meanwhile, during a period of broad USD strength, SGD remains one of the best performing Asian currencies. Given Singapore’s solid economy and robust fiscal position, these trends are likely to persist. The MAS strengthening of the S$NEER may moderate the upward direction of interest rates over the medium term, but a hawkish Fed suggests yields are likely to remain elevated for the foreseeable future.

Unless otherwise stated, all data sources are from the Monetary Authority of Singapore and J.P. Morgan Asset Management as of 14 October 2022.