A “close call” on the BOE’s laboured path to higher rates

08-11-2021

Olivia Maguire

IN BRIEF

- The Bank of England (BoE) went against market expectations for a rate hike as they left the Bank Rate unchanged at 0.1% and maintained total target of asset purchases at GBP 895 billion.

- Higher inflation is still considered transitory by the Monetary Policy Committee (MPC) but they indicated if upcoming labour market data is in line with central projections then Bank Rate will rise in coming months.

- The deferred hike means no immediate respite to ultra-low sterling yields, although further interest rate volatility is likely; investors should consider maintaining a disciplined approach to cash investment and segmentation.

Cold water was thrown on the fevered market speculation that the BoE would become the first major-developed market central bank to hike rates as the MPC reneged on expectations and voted 7-2 to leave interest rates unchanged at 0.1%. Concurrently, the MPC voted 6-3 to maintain the total target of asset purchases at GBP 895 billion (GBP 875 billion of government bonds and GBP 20 billion of corporate bonds). This postponement of post-COVID normalisation of monetary policy has significant impact for short-term investors.

A volte-face by the “Old Lady of Threadneedle Street”?

The recent stronger than expected economic data, combined with higher than anticipated inflation, had increased market expectations that the BoE would hike rates at the November meeting. Hawkish rhetoric and explicit signals from MPC members - that they would intervene if they saw upside risks to medium-term inflation expectations - meant the market was primed for immediate central bank action. Therefore, the decision to leave rates unchanged at the meeting - described as “a very close call” by BoE Governor Andrew Bailey - wrong-footed the market and magnified the markets’ scepticism regarding the BoE’s communication credibility.

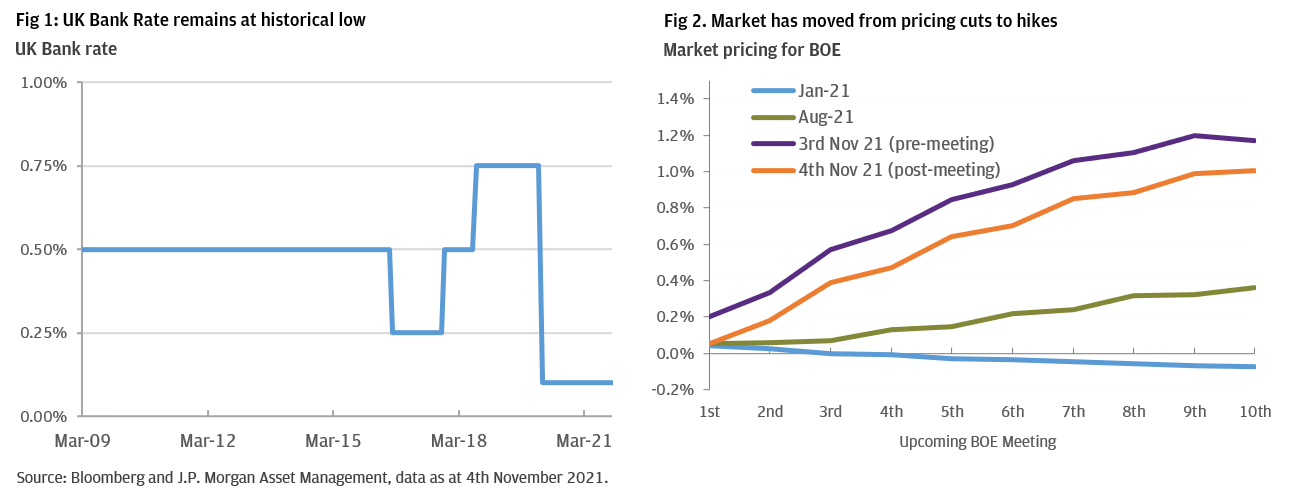

The MPC’s decision leaves interest rates at the historically low levels which have prevailed since Bank Rate was slashed from 0.75% to 0.1% in March 2020 in response to the pandemic (Fig 1). Nevertheless, the recent bond market movements – even after today’s repricing – represent a dramatic pivot from expectations at the beginning of the year when negative interest rates seemed highly probable (Fig 2).

Patience: Labour data is the key

Explaining its rationale, the BoE recognised that the rapid rollout of vaccines and lifting of COVID lockdowns had triggered a strong rebound in aggregate demand that supported a robust economic recovery. Despite supply bottlenecks, the central bank forecasts GDP will return to pre-COVID levels in Q1 2022. However, growth momentum will ease over the medium term as energy price increases bite and looser financial conditions fade; growth in 2022 and 2023 are estimated to be 5% and 1.5% respectively.

The BOE also noted that the labour market has been strong. Unemployment is lower than expected and continues to fall, but is still higher than before the pandemic; whilst near-term uncertainty, relating to the ending of the furlough scheme, remains. The BoE is clearly waiting for the additional employment data due before their December 16th meeting. Should this data delivers in line with their expectations, the MPC confirmed it would “be necessary over coming months to increase Bank Rate” in order to return Consumer Price Index (CPI) inflation sustainably to the 2% target.

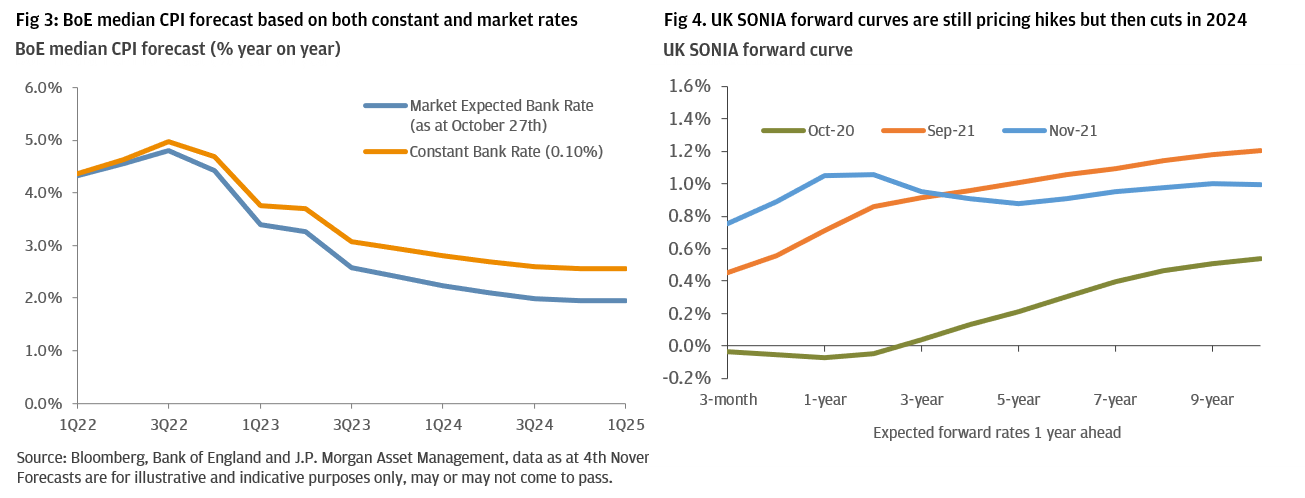

The latest forecasts in the November Monetary Policy Report (MPR) do suggest that median CPI inflation is expected to overshoot the BoE’s 2% target based on an unchanged Bank Rate (Fig 3). This is a clear sign that the current inflationary pressures may not be as transitory as first expected. However, according to the implied market path for interest rates, the BoE projects that inflation will return to just below target over the medium term.

Investor Implications

Sterling cash investors, grappling with low yields since March 2020 will have to wait a little longer for the rate increase that delivers higher cash yields and leaves negative rate fears behind. Forward SONIA curves continue to imply near-term rate hikes are likely, and that the Bank Rate will reach a terminal level of 1% by the end of 2023 to prevent inflation becoming embedded (Fig 4). However, these same curves have started to price in rate cuts during 2024 as a reflection of uncertainty for long-term growth.

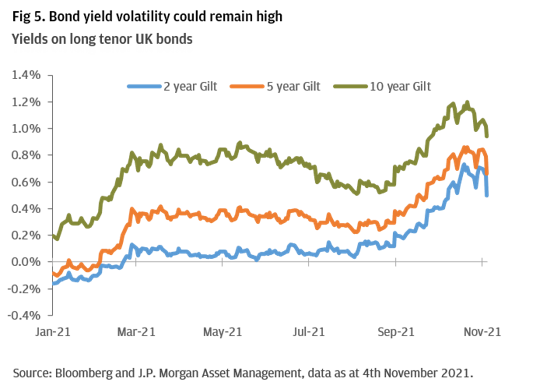

This conflict between inflation and growth suggests bond yield volatility could remain high, although longer term bond yields are likely to continue increasing over the medium term (Fig 5). Given the increased risk of capital losses on longer duration strategies, Sterling investors should consider adopting a disciplined approach to cash segmentation. By prioritising a combination of money market and ultra-short duration strategies, this should allow investors to optimise returns without excessively increasing risk or volatility.

09sg210311081756