In brief

- The RBA hiked base rates by 25 bps to 4.10% for a second straight meeting as inflation re accelerates and short term expectations rise with risks “tilted further to the upside.”.

- Greater capacity pressures, stronger private demand, a tight labour market and Middle East energy risks drove the hike; despite a split vote and data dependence, the RBA’s commentary stayed hawkish.

- For AUD cash investors, the rate hike is positive news, offering higher yields while hawkish guidance should keep the yield curve steep – presenting opportunities to selectively extend duration to lock in yields.

Introduction

At its March meeting, the Reserve Bank of Australia raised the cash rate target by 25bps to 4.10%, acknowledging that while inflation has declined from its peak, it “picked up materially in the second half of 2025” and that short term inflation expectations have already risen. The Board judged there is “a material risk that inflation will remain above target for longer than previously anticipated,” citing emerging capacity pressures and external shocks from sharply higher fuel prices linked to the Middle East conflict.

This decision extends February’s hawkish pivot and underscores the RBA’s readiness to act pre emptively to contain upside risks—a stance consistent with its recent messaging that inflation pressures had become broader and more persistent than anticipated.

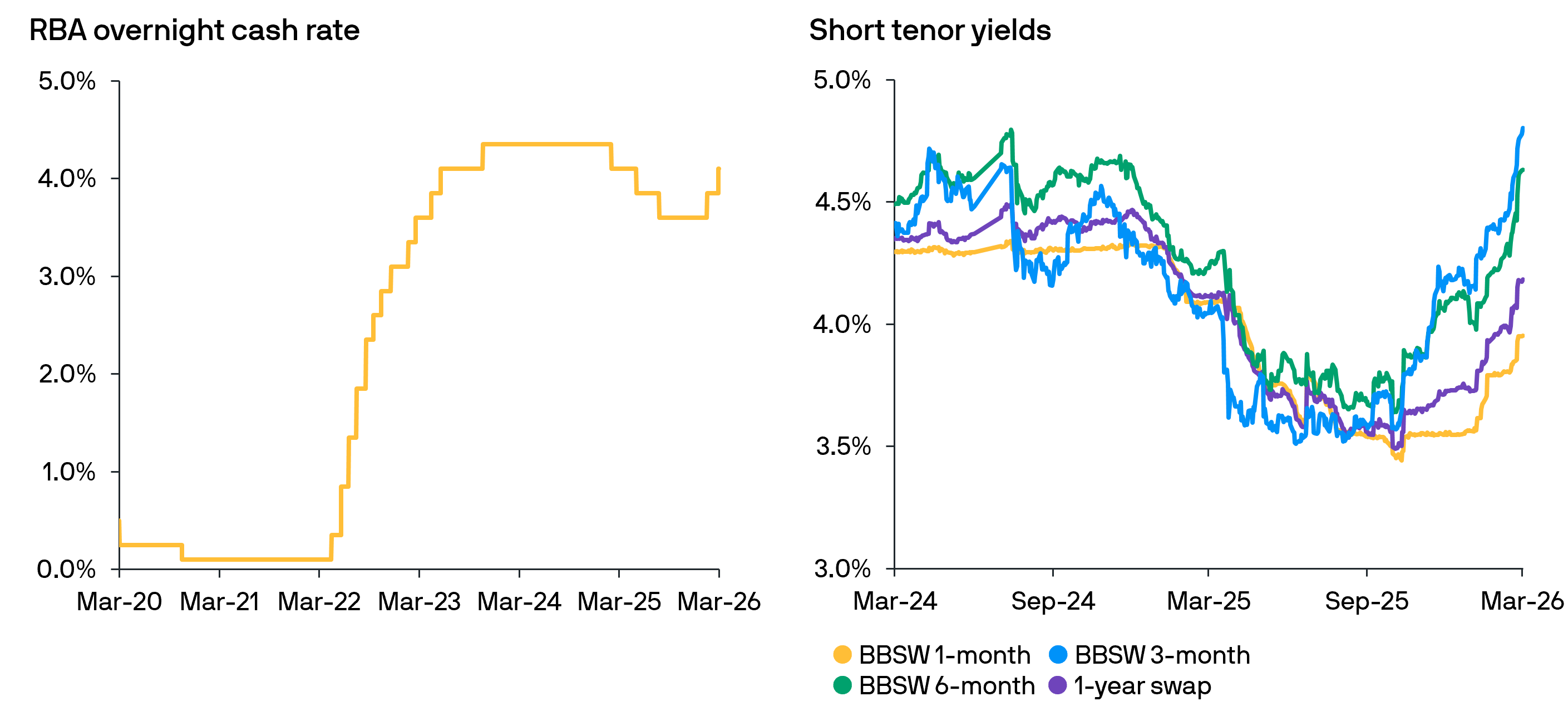

Fig 1: RBA has hiked twice in the current cycle pushing market yields higher and curve steeper.

Source: RBA, Bloomberg and J.P. Morgan Asset Management; data as of 17 March 2026

Capacity limitation

The RBA’s statement highlighted two key inflation drivers: renewed domestic capacity pressures and external energy shocks. On domestic factors, the bank noted that “some of the increase in inflation reflects greater capacity pressures” with the labour market remaining tight and the unemployment rate “a little lower than expected,”. Strong housing activity and prices were another sign of demand resilience, while business investment and overall demand was “substantially more than was expected in mid 2025”. For the RBA, these trends question “the extent to which monetary policy is restrictive,”.

On external energy shocks, mounting risks from the Middle East conflict, has “resulted in sharply higher fuel prices, which, if sustained, will add to inflation”. Critically, “short term measures of inflation expectations have already risen,” raising the risk that above target inflation persists longer than expected. The Board further cautioned that a “longer or more severe conflict could put further upward pressure on global energy prices,” potentially embedding higher inflation expectations.

Conclusion and Rate Outlook

The Board’s decision passed by a narrow majority—five for a hike, four for no change—signals a robust debate rather than concerns about a potential policy mistake – especially with inflation risks still “tilted further to the upside”. This was confirmed by Governor Bullock’s hawkish remarks that “inflation was already too high” and the “cash rate was not consistent with CPI returning to target”, which should maintain upward pressure on yields.

While the RBA confirmed it will “be attentive to the data,” as it pursues “price stability and full employment”, they also committed to “do what it considers necessary” to return inflation sustainably to target. In practical terms, back to back hikes reinforce a higher for longer bias while energy driven pressures and capacity constraints persist; however, if earlier tightening curbs inflation, the RBA could revert to a steady hold sooner.

For AUD cash investors, the rate hike is positive news, presenting higher yield opportunities while hawkish guidance should keep the yield curve steep – creating scope to selectively extend duration to lock in yields.