We think AI will lead to all sorts of business transformation and productivity gains in the long term, but recent performance has been driven by significant upgrades in near-term AI demand projections.

In brief

- Concerns over market concentration in the S&P 500 have once again returned and raised concerns over a potential bubble.

- The good news is, the market leaders are more profitable than the ones that led the dot-com bubble, fundamentals remain strong and they are boosting shareholder returns.

- Risks remain surrounding the sustainability of artificial intelligence (AI) demand and its costs. Investors should continue to stay diversified and focus on fundamentals.

The economy and the stock market are not always playing to the same tune. In today’s financial market ensemble, a stable economy plays a familiar melody with some nuance around rate cuts. Meanwhile, AI has staged a dramatic crescendo—perhaps lasting too long for comfort.

The S&P 500 is up a stellar 45.8% since the start of 2023, but subtracting just one name from the index, Nvidia, cuts that return to 37.4%. Subtracting the top five names further reduces that return to 23.4%. While impressive tech performance has boosted the overall market, excessive stock rallies and 31 new all-time highs this year have raised concerns about a potential bubble.

However, there are reasons to believe this isn’t the case.

1. Risk appetite. During the dotcom bubble, rampant speculation surrounded young companies flaunting internet excitement before profitability. In contrast, today’s AI beneficiaries are already very profitable companies that make their money selling key infrastructure and resources to the rapidly growing market of AI adopters. Additionally, interest rates are high, initial public offerings have slowed to a trickle and global venture capital investments have fallen from their peak in 20211. While bullish sentiment has surely provided a boost2, the impact of earnings upgrades is likely more significant—the Magnificent 7 posted a remarkable +50% year-over-year earnings growth in 1Q24.

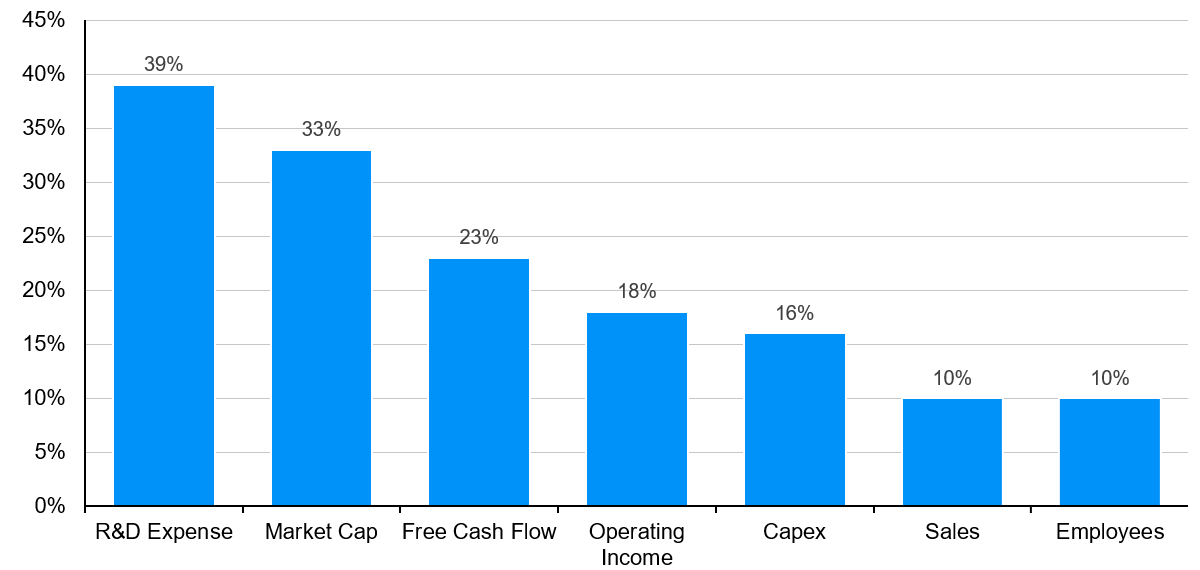

2. Fundamentals. The Magnificent 7 account for a sizable 33% of market cap, but they also account for 39% of R&D spending, 23% of free cash flow and 16% of capex (see Exhibit 1). The strongest are getting stronger, but they’re fueled on veggies and complex carbs, not short-term stimulants.

3. Shareholder return. The recent boost in shareholder return can also be attributed to tech strength. Certain mega-cap tech companies have announced substantial share buyback programs or first-ever dividend payouts this year. These announcements have contributed to a 6% increase in S&P 500 shareholder payout in 1Q24, and the S&P return-on-common-equity stands at a solid 18.5%.

Exhibit 1: Market concentration is an issue of economic concentration

Magnificent 7 stocks, % share of S&P 500 on specific metrics

Source: Bloomberg, J.P. Morgan Asset Management. Magnificent 7 includes AAPL, AMZN, GOOG, GOOGL, META, MSFT, NVDA and TSLA. Data reflect most recently available as of 21/06/24.

Source: Bloomberg, J.P. Morgan Asset Management. Magnificent 7 includes AAPL, AMZN, GOOG, GOOGL, META, MSFT, NVDA and TSLA. Data reflect most recently available as of 21/06/24.

Still, there are reasons to be cautious. Markets have a tendency to over-appreciate the near term and under-appreciate the long term. We think AI will lead to all sorts of business transformation and productivity gains in the long term, but recent performance has been driven by significant upgrades in near-term AI demand projections. If demand cools off unexpectedly, perhaps because the economy deteriorates, geopolitics, or capacity constraints become a binding factor, such projections could be overly optimistic. Further, pricing discovery is in its nascency and the costs to run complex large language models (LLMs) are still massive. Once ChatGPT becomes integrated to your iPhone, how much would you pay for the premium subscription? How much should a small business pay for Microsoft’s CoPilot suite? If we moved the nine billion daily searches in Google onto Chat-GPT today, could we supply a 10x increase in electricity demand3?

Investment implications

The alarm bells may not be ringing like the dotcom bubble. Concentration today appears to showcase corporate resiliency and companies that are at the forefront of growth, but questions abound whether recent performance can be sustained. As such, investors can still enhance diversification by exploring overlooked areas of the market, within and outside of the AI value chain, that have strong fundamentals.