Broadening profit growth this year should highlight plenty of attractive opportunities across the market.

In brief

- U.S. 1Q24 earnings have been better than expected.

- Companies are expanding margins, and any success moving forward will depend on their ability to keep doing so.

- Broadening profit growth should present opportunities outside of the Magnificent 7.

- Earnings growth is set to accelerate through the rest of the year.

Slowing, but still growing

During the first quarter, U.S. equities shrugged off ever-changing expectations for monetary policy with relative ease, climbing 10.6% despite a sharp hawkish repricing in policy expectations. However, an unexpected jump in inflation in March sparked the resurgence of the “higher for longer” narrative, leaving equity valuations elevated, and vulnerable, at the onset of the 1Q24 earnings season.

While the U.S. economy slowed in 1Q24, a 2.5% quarter-over-quarter annualized increase in consumer spending pointed to a healthy underlying momentum. This, along with solid inflation, have supported profit growth on an annual basis in this earnings season. Revenues have benefitted from higher prices, while companies have had success expanding margins despite recent geopolitical headwinds. As of May 10, 50% of companies have delivered upside surprises on revenues and 73% have beaten earnings forecasts, both of which are in-line with their long-run averages, and surprises for both measures have been positive on an average.

With 88% of market cap having reported earnings, results thus far have been solid. Analysts’ estimates for pro-forma earnings per share (EPS) are currently tracking at $55.29, which would represent an increase of 5.3% year-over-year and 1.1% quarter-over-quarter, if realized. Margins are expected to do the bulk of the heavy lifting, while share buybacks are set to detract 0.4% points from growth.

As inflation and consumer demand moderate in the coming quarters, more onus will fall on margins to maintain profit growth, although monitoring revenues will be increasingly important as pricing power diverges across companies. While slowing wage inflation and moderating input costs suggest the worst of margin pressure is behind us, there are risks that could keep costs elevated. As companies focus on maintaining margins despite this, the increased utilization of artificial intelligence (AI) within business processes should support the cause

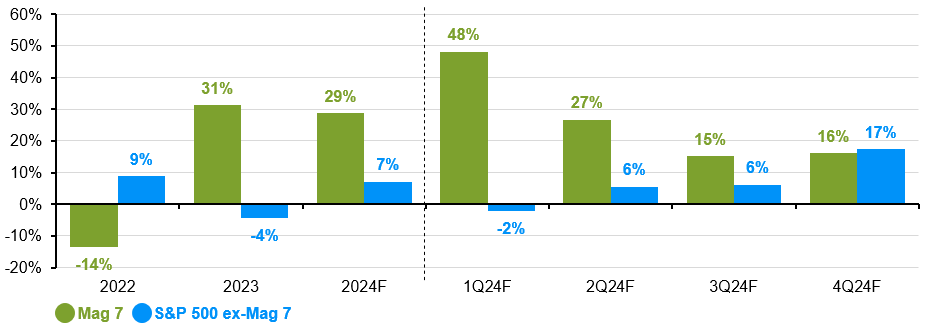

Earnings growth should broaden beyond the Magnificent 7*

Pro-forma EPS, year-over-year percentage change

Source: FactSet, Standard & Poor's, J.P. Morgan Asset Management. Data are as of May 2, 2024

*Magnificent 7 includes AAPL, AMZN, GOOG, GOOGL, META, MSFT, NVDA and TSLA. Earnings estimates for 2024 are forecasts based on consensus analyst expectations.

Growth sectors continue to lead the charge

Similar to last quarter, growth sectors will likely drive the bulk of pro-forma profit growth, while cyclicals look more mixed. Information technology and communication services should continue to reap the benefits of prudent expense management and demand for AI capabilities, while resilient consumer demand has supported the consumer discretionary sector. Elsewhere, financials and industrials are on track to improve, while materials and health care are anticipated to see earnings contract by over 20% year-over-year. Moreover, lower natural gas prices in 1Q will likely hamper results in the energy sector.

The market’s response to the Magnificent 7, which are projected to dominate earnings growth once again this quarter (+48% year-over-year vs. -3% year-over-year for the rest of the index), has been increasingly driven by sentiment. On average, companies delivering beats within this cohort are down in the trading day after earnings, while the one company that missed expectations jumped by more than 4%. In our opinion, the divergence between price movement and fundamentals suggests some fragility within the market, particularly within the Magnificent 7. That said, broadening profit growth this year should highlight plenty of attractive opportunities across the market.

Investors deterred by recent volatility and the cloudy economic outlook should not fret. Even after a solid first quarter, earnings are only expected to improve from here, with every other quarter on pace to deliver both sequential and annual growth. What is even more promising for investors, however, is that if this trend persists, all 11 S&P 500 sectors could see earnings grow on a year-over-year basis by the fourth quarter, a feat that has not been achieved since 2Q21.

Investment implications

While nominal growth remains supportive, it will likely trend lower through the balance of the year, putting more focus on margins as a driver of profit growth. Against a backdrop of elevated valuations and moderating economic activity, we maintain a bias towards quality. This means a preference for large caps over small caps, and an increased focus on finding companies with positive fundamentals that can back current multiples.

Moreover, as profit growth expands outside of the Magnificent 7, investors should search for opportunities across sectors, especially those that are seeing renewed earnings tailwinds after a period of weakness.