The committee will be cautious about cutting interest rates prematurely if growth remains strong and labor markets remain tight.

As widely anticipated, the Federal Open Market Committee (FOMC) voted to leave the Federal funds rate unchanged at a target range of 5.25%-5.50%. The statement language was largely unchanged, with slight adjustments acknowledging the recent strength of the labor market. The statement continues to highlight that inflation has eased but remains elevated.

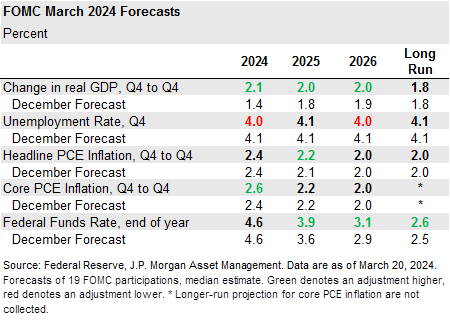

Updates to the Summary of Economic Projections further signaled a rosier outlook for the economy in the year ahead. Relative to the committee’s December forecast:

- Real GDP growth was upgraded meaningfully from 1.4% to above-trend growth of 2.1% for 2024. Estimates for 2025 and 2026 were also revised higher.

- Unemployment rate projections were revised down to 4.0% in both 2024 and 2026.

- While headline personal consumption expenditures (PCE) projections for this year were unchanged at 2.4%, core PCE was lifted to 2.6%. Headline inflation forecasts for 2025 were modestly adjusted higher.

- Notably, policy rate projections (dot plot) continued to signal three rate cuts this year, with no committee member anticipating any further hikes, but a downward revised three cuts in 2025. Projections for the longer-term federal funds rate ticked higher to 2.6%, suggesting that the committee’s assessment of a “neutral” rate is rising.

Investors should not be too surprised with today’s announcement. So far this year, the data continue to reflect a healthy labor market, good overall economic activity and inflation still on a downtrend, though it could take a bit longer to reach target. Importantly, there is still a clear bias to cut rates from the committee.

At the press conference, Federal Reserve (Fed) Chairman Jerome Powell emphasized this message; the committee views current policy rates as restrictive, which should allow inflation to return to trend over time. That said, the committee will be cautious about cutting interest rates prematurely if growth remains strong and labor markets remain tight. When asked about the balance sheet, Chairman Powell indicated that a decision to slow quantitative tightening would be made “fairly soon,” as a slower pace of balance sheet reduction would reduce the risk of short-term rate volatility bringing quantitative tightening to a premature end. We stick to our base case for three rate reductions this year beginning in June. With three more Consumer Price Index prints before the June meeting, there should be more evidence inflation is still on a very gradual downward path.

09h2242103011759