The Reserve Bank of Australia’s Crisis of Confidence

04/11/2021

Aidan Shevlin

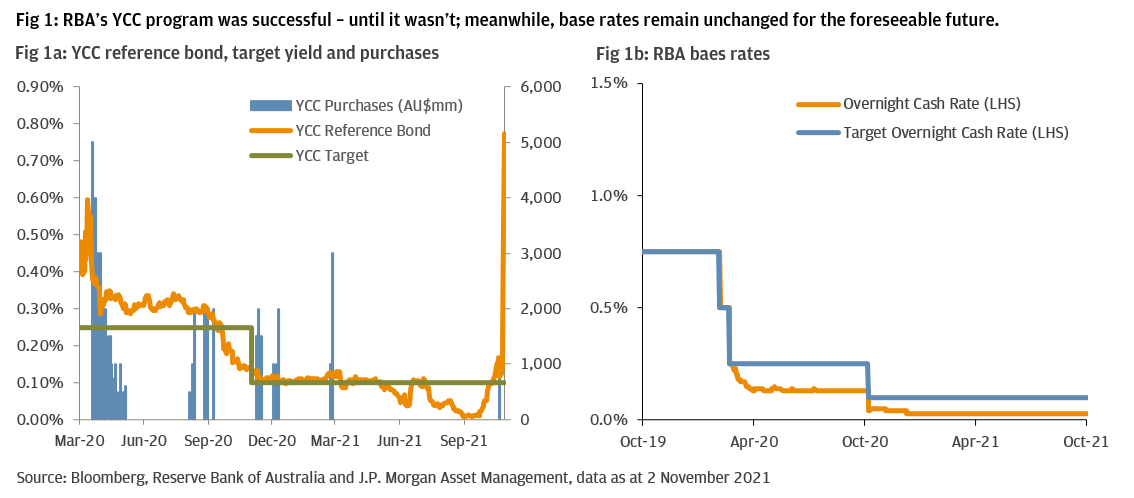

During October, the yield on the RBA’s yield curve control (YCC) target reference bond spiraled upwards and closed at 0.775%, well beyond the central bank’s 0.10% target. This was an unexpected reversal for a bond which was historically very stable with minimal central bank interventions, since the RBA first introduced the YCC program in March 2020.

A combination of increasingly positive economic momentum and higher than expected inflation were the kindling, while the RBA’s failure to support its target rate was the spark. Both factors have pushed yields across the curve significantly higher and forced the central bank into a dramatic volte face at their November monetary policy meeting. This event will have significant implications for AUD cash investment strategies.

Abandoning the anchor:

In March 2020, the RBA announced a new YCC program and committed to keep the yield on the 3-year government bond yield “around its target level” by purchasing a mixture of government and semi-government bonds. Since then, the central bank has purchased a total of AUD 80bn via this program, including over AUD 20bn of the target “on-the-run” ACGB1 2.75% April 2024 bond, representing 63% of the total bond outstanding.

With stable yields on the reference bond, the RBA’s requirement to purchase YCC bonds dwindled. Although, as recently as its October monetary policy meeting, the RBA remained committed to its 0.10% YCC target and to keeping base rates unchanged until 2024.

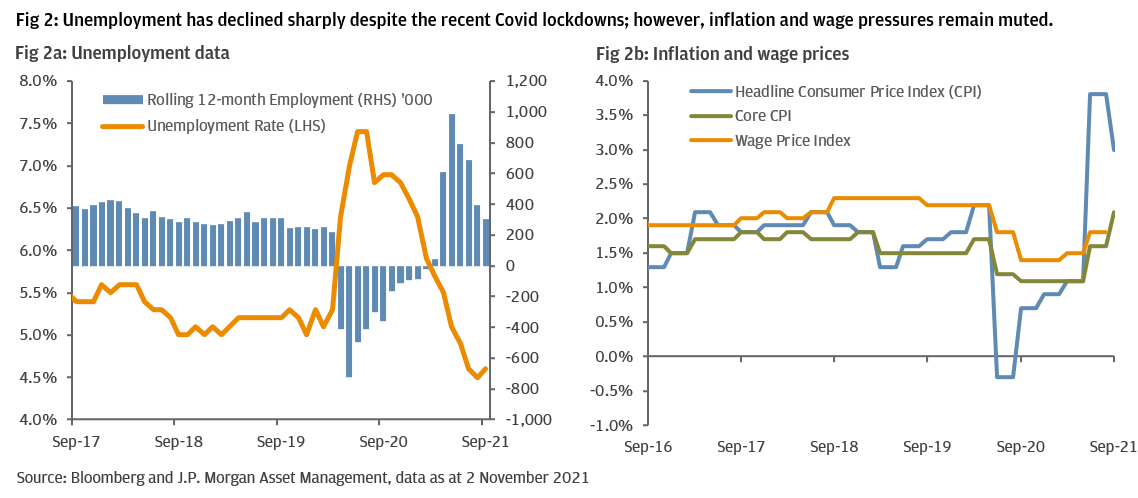

However, the recent reopening of Melbourne and Sydney economies, together with better than expected global economic data pivoted the balance of risks to the upside. Subsequently, inflation concerns were magnified as Q3-21 core inflation jumped to 2.1%y/y, within the RBA’s target range for the first time in six years. The stark contrast between better than expected data and the RBA’s still very dovish comments suggested the central bank was behind the curve and triggered a market sell-off, as economists anticipated an unavoidable adjustment to RBA’s forward guidance was imminent.

AUD bond yields soared higher in late October and the RBA’s failure to defend its 0.10% YCC target acknowledged that the program was no longer fit for purpose and was impacting market functioning.

Acquiescing to market pressure at its November monetary policy meeting, the RBA justified discontinuing the YCC program by explained the decision “reflects improvements in the economy and earlier than expected progress towards the inflation target”. Noting that, “bond yields have increased recently and bond market volatility has also risen significantly”, the central bank accepted “the effectiveness of the yield target has diminished”.

Enforced hawkish pivot:

In addition to scrapping its YCC program, the RBA confirmed its current cash rate target and the continuation of its QE program. It also switched to data dependent forward guidance while revising its inflation and unemployment forecasts higher.

The failure to scale back its QE program disappointed investors looking for signs of a 2022 rate hike. Whilst the RBA did note that core inflation “had recently picked up”, hitting a six-year high of 2.1%y/y; it is still only at the bottom of the central bank’s 2% to 3% target range. This allowed the central bank to remain “committed to maintaining highly supportive monetary conditions”, until “actual inflation” is consistently within the target range and the unemployment rate falls sufficiently to generate sustainable wage growth. Nevertheless, the upgraded economic outlook effectively signaled that rate hikes are possible by 2023, much earlier than the previous 2024 guidance.

Market and investment implications

Following the RBA’s announcement, the market unwound expectations of an early 2022 rate hike. As a result, the AUD fell, bond yields declined and the curve flattened. Nevertheless, interest rates remain significantly higher than four weeks ago and should continue to trend upwards as investors digested the central bank’s rapid policy pivot from dovish to hawkish within the space of one meeting. The divergence between RBA’s forecasts and its requirement to see actual data before adjusting policy rates also remains a point of contention, implying higher market volatility is likely.

Australian government bonds recorded losses in September and October, leaving indices negative for the first year since 2009. However, the rapid upward movement of Australian interest rates has also created investment opportunities.

For AUD overnight cash investment, deposit and repo rates are unlikely to increase until the RBA eventually hikes rates. In contrast, for money market and ultra-short duration strategies, the rebound in market yields will be welcome after an extended period of close to zero returns – allowing for higher reinvestment and broader yield diversification. Nevertheless, a disciplined and diversified investment strategy remains critical to optimize returns while minimizing the probability of suffering opportunity costs.

1 Australian Commonwealth Government Bonds

Diversification does not guarantee investment returns and does not eliminate the risk of loss.