The PBOC's reluctant policy pivot - another 50bps Reserve Requirement Ratio cut

09/12/2021

On December 7, the PBoC announced an unexpected 50bps Reserve Requirement Ratio (RRR) cut. The broad based cut will release significant liquidity into the financial system, while the resultant confirmation that policymakers are focused on stabilizing growth has boosted investor sentiment. CNY cash investors should pay attention to the PBoC’s rapid pivot from neutral to dovish monetary policy and the implications.

Marginal Monetary Impact:

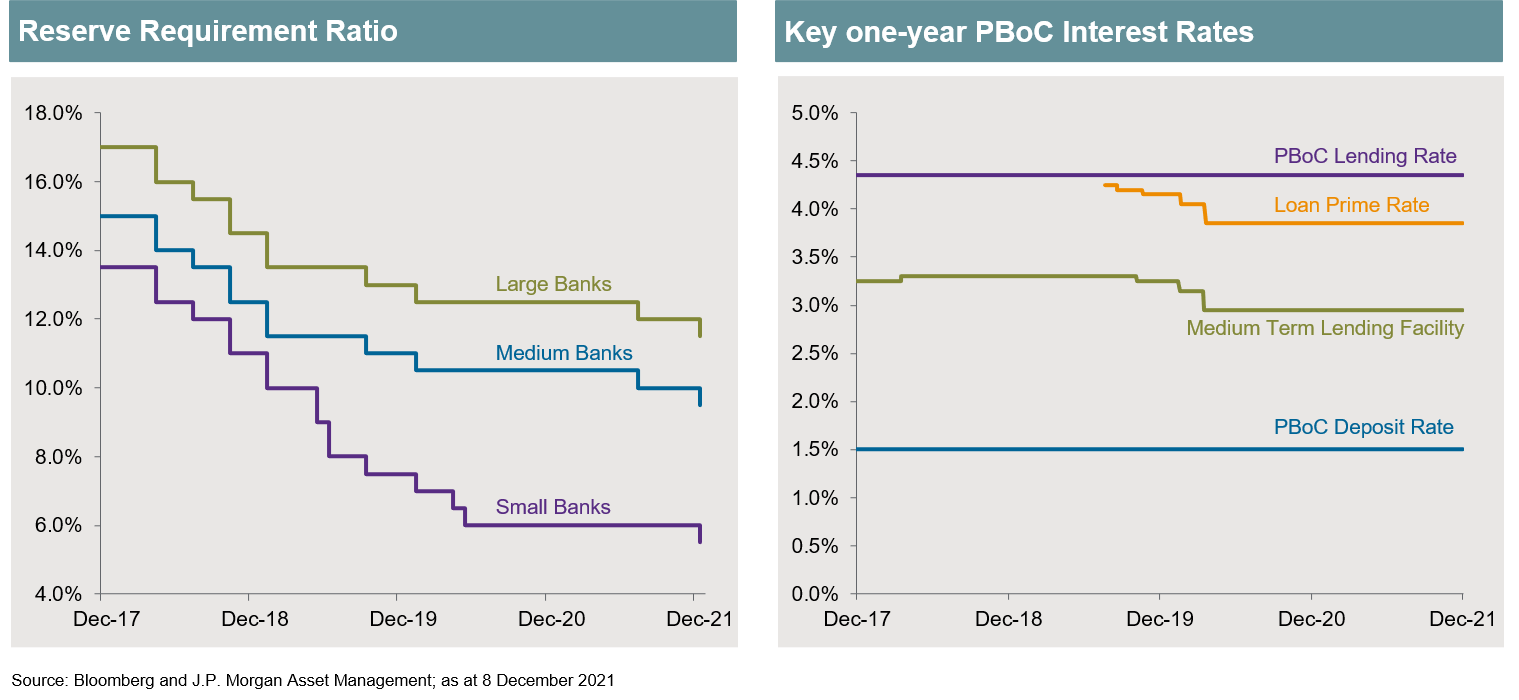

The latest RRR cut will reduce the ratio for large, medium and smaller banks to 11.5%, 9.5% and 5.5% respectively (Fig 1a). Some rural banks already enjoy lower RRR rates, although PBoC comments suggest the floor for the ratio will be 5%. Other PBoC quasi-monetary policy interest rates have remained unchanged (Fig 1b) since the first quarter of 2020, with the central bank favouring open-market-operations to maintain market stability and liquidity.

Fig 1: The PBoC announced the second broad based RRR cut of 2021; however other key interest rates remain unchanged.

The PBoC confirmed the intention of RRR cut was two-folded – increasing bank funding to support the economy, especially small and medium-sized enterprises (SMEs), and lowering financial institutions funding costs which could help lower costs for the economy. They estimates the rate cut will release approximately RMB1.2trn of permanent liquidity into the banking system, helping offset CNY950bn of Medium-Term Lending Facility (MLF) maturing in December. The central bank also indicated that the RRR cut would reduce bank funding costs by approximately CNY15bn, however, given the total deposit base is approximately CNY230trn, which only implies a 0.07% reduction in funding costs.

Following the rate cut, the PBoC stated it would "keep a stable and normal monetary policy stance, avoid flooding the economy with liquidity, and maintain internal and external balances”, suggesting additional aggressive rate cuts are unlikely in the near term.

Positive Policy Impact:

This is the second RRR cut in 2021 and similar to the previous RRR cut on July 9, it was foreshadowed by calls by Premier Li for ‘RRR cut at an approximate time in order to keep liquidity reasonably ample and increase support for the real economy, especially SMEs”.

Weaker than expected economic data, combined with power outages and property market stresses had raised expectations of further monetary policy easing. However, as recently as October, the PBoC suggested no further rate cuts were likely, so the rapid pivot surprised the market, which did not expect further monetary policy intervention until next year.

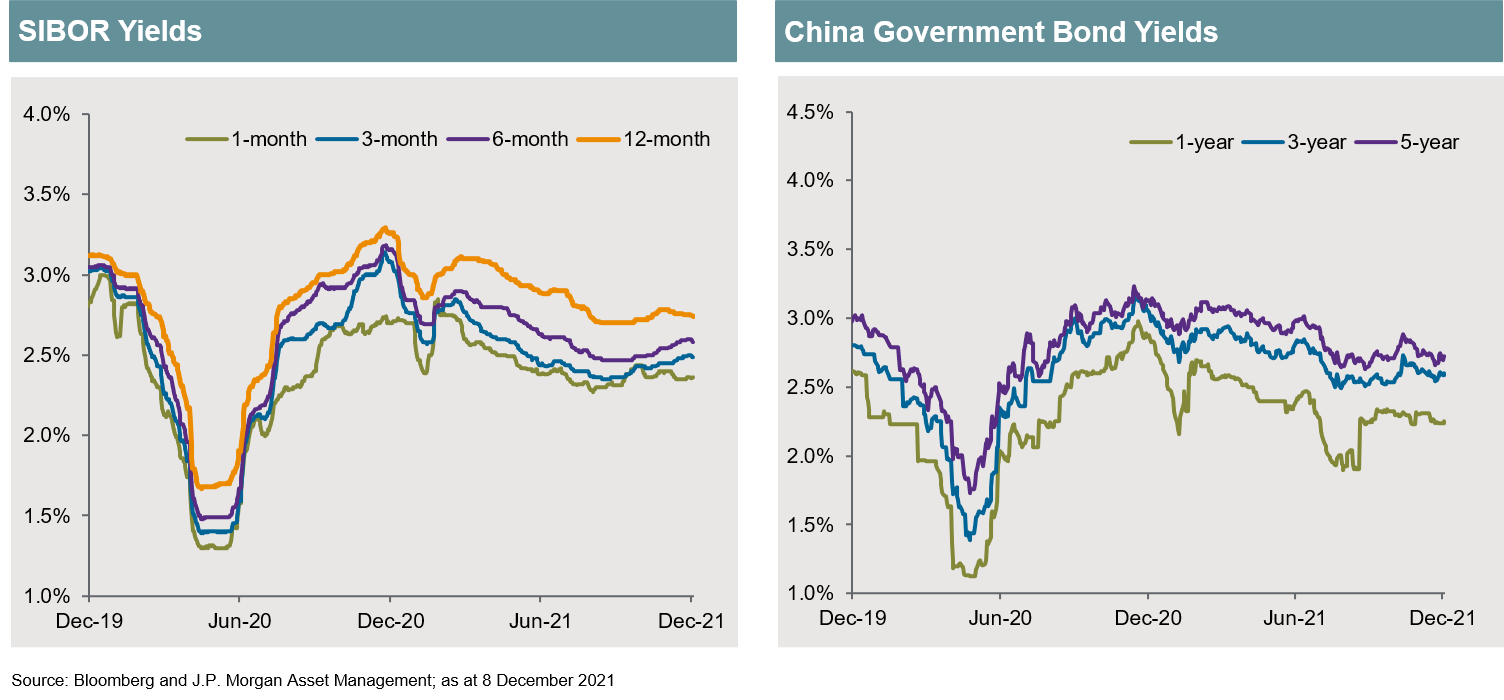

Following Premier Li’s comments, bond yields declined and the yield curve flattened (Fig 2), with this trend extending after the PBoC announcement.

Fig 2: SHIBOR and longer term bond yields declined and the curve flattened following Premier Li’s comments

Concurrently, at their regular meeting on December 6, the Politburo confirmed the need to support the property market, stabilize growth and boost domestic demand. This suggests the Central Economic Work Conference will be more supportive as key policymakers confirm economic stabilization as the top priority.

Conclusion: Pivot to stabilization

As economists contemplate slower Chinese economic growth in 2022, confirmation that the authorities are focused on stabilizing economic growth has assuaged concerns of a rapid deceleration.

The more dovish tone emanating from the Politburo meeting, combined with the comments from Premier Li and subsequent rate cut by the PBoC, delivered a positive signal that monetary policy has turned dovish, which should help reassure financial markets and boost economic sentiment.

They have also heightened expectations of additional RRR and other monetary policy rate cuts next year. For CNY cash investors, the prospect of a more dovish PBoC suggests a diversified cash investment strategy – across different maturities and strategies that can extend duration – is critical to optimizing returns.

Diversification does not guarantee investment returns and does not eliminate the risk of loss.