Contrasting with the U.S., the dilemma between growth and inflation is less profound for other developed markets central banks, and hence the rate cut cycle may come later.

In brief

- Weak growth and banking sector stress could persuade the Fed to consider policy loosening before year-end, despite still elevated inflation

- Other developed market and Asian central banks are also approaching peak policy rates, but may not be in a rush to ease

- The investment playbook after the end of Fed hiking cycle is similar to one that prepares for a recession – long duration, investment grade fixed income and quality and defensive stocks

At the start of the year, we argued that 2023 would be more challenging for central bankers around the world. Instead of just raising rates aggressively to cool inflation against a strong economic backdrop, they now need to balance their monetary policy between stubborn inflation and a greater risk of economic recession and financial sector shocks. The analogy we used then was of a fast car speeding down a straight road, but are now facing a number of sharp corners ahead. We think most central banks will reach the end of their hiking cycles in the months ahead. The question of whether they will start cutting is a more challenging one.

The Fed’s tough stance on inflation may need to change

There are several reasons to think the Federal Reserve (Fed) ended the rate hiking cycle at its recent May FOMC meeting, in addition to the comments in the statement. The policy rate is now consistent with the peak policy rate predicted in the March FOMC forecasts. Moreover, there are growing signs that the economy is facing more headwinds from the regional banking sector's stress. In the Fed’s latest financial stability report, it highlighted that banks and financial institutions are looking to contract credit supply to the economy. This tightening of lending standards, which historically has appeared before recessions, is also reflected in the latest release of the Senior Loan Officer Survey.

This would put more pressure on the economy, even though the job market is still solid and consumption is in good shape. A reduction in corporate spending and a weaker housing market could put further pressure on the Fed to loosen monetary policy later in the year, even if inflation is slow to come down. The latest political drama on raising the federal government debt ceiling is also going to impact on confidence. Currently, the market is pricing 100bps of rate cuts by the January 2024 meeting with the first cut to come in September. This expectation could be built upon previous rate cycles where the average period of the last hike to the first cut is around 6 months. That said, historical precedents may be less applicable now with inflation being still the top priority for the Fed.

Other central banks could stay hawkish for now

Other developed market central banks have less of a problem with their banking sectors, while inflation has yet to show convincing signs of coming down. Both the European Central Bank (ECB) and the Bank of England raised their policy rates by 25bps in the past two weeks. The eurozone economy has been surprisingly resilient, despite the energy challenge of 2022. This gives the ECB the confidence to tighten. For the UK, its March year-on-year inflation is still in double digits, at 10.1%. The Reserve Bank of Australia also surprised the market by raising its policy rate by 25bps in its May meeting, following a pause in April.

Contrasting with the U.S., the dilemma between growth and inflation is less profound for other developed markets central banks, and hence the rate cut cycle may come later. This could also put more pressure on the U.S. dollar as rate differentials widen.

In Asia, South Korea, India and Indonesia all kept their policy rates unchanged in their most recent meetings. Malaysia’s central bank surprised the market with a 25bps increase. The challenges for Asian central banks is that domestic demand is recovering and the labor shortage seen in the west is also taking place in this part of the world. Hence, it remains to be seen whether demand-led inflation could prompt Asian policy makers to stay hawkish. Meanwhile, export demand remains weak and some of the positive impact from higher commodity prices are fading for raw material exporters, such as Malaysia and Indonesia. On balance, we see most Asian central banks to also opting to pause this summer, partly because they have been proactive in tightening policies last year.

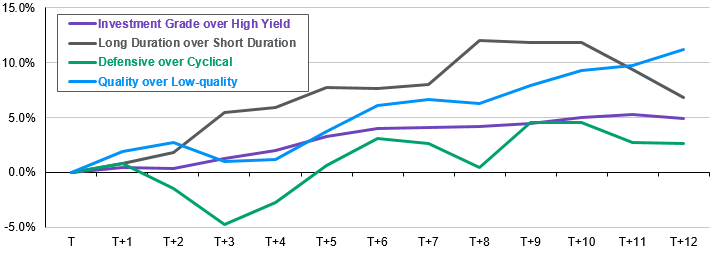

Exhibit 1: Cumulative outperformance after final Fed rate hike in a cycle

Average cumulative outperformance, total return, T = month in which the last rate hike occurred

Source: Bloomberg, MSCI, Standard & Poor's, J.P. Morgan Asset Management. Investment Grade: Bloomberg US Corporate Bond Index, High Yield: Bloomberg US Corporate High Yield Bond Index, Long Duration: Bloomberg US Long Treasury Index, Short Duration: Bloomberg US Short Treasury Index, Defensive: MCSI Defensive Sectors Index, Cyclical: MSCI Cyclical Sectors Index, Quality: S&P 500 Quality Index, Low-quality: S&P 500 Quality - Lowest Quintile Index. Due to data availability, Investment Grade over High Yield averages outperformance from the past 6 rate hiking cycles, Duration over Short Duration averages outperformance from the past 5 rate hiking cycles, Quality over Low-quality averages outperformance from the past 4 rate hiking cycles, and Defensive over Cyclical averages outperformance from the past 3 rate hiking cycles. The calculations are based off of monthly returns, and begin at the month-end price for the month in which the last rate hike occurred. Data reflect most recently available as of 03/05/23.

Investment implications

Historically, a pause by the Fed has several investment trends that we can take note of. First, long duration assets have outperformed short duration. This is partly because investors start to position for an economic slowdown and this could see long end of the yield curve dip more than the short end. As we have been recommending for much of this year, investment grade corporate debt has outperformed high yield. The prospects of weaker growth could raise default rates and widen credit spreads. This would have a more significant impact on high yield bond price than investment grade. High quality stocks and defensive sectors are also expected to outperform. This is again linked to the prospects of weaker growth.

The peaking of policy rates in other parts of the world should also bode well for long duration fixed income in international government bonds. The fact that the Fed will likely lead in rate cuts has already put pressure on the U.S. dollar. This also in turns benefit Asian and emerging market assets.