Asia credit valuations look reasonable, while offering attractive carry at the same time.

In brief

- At the moment, investors are cautious to add risk to Asia credit due to global macro uncertainties

- However, Asian economies are experiencing growth tailwinds, Asian central banks are nearing the end of rate hike cycles and Asian currencies are strengthening, limiting the downside risks.

- Yields in Asia credit are attractive and we prefer a quality bias. Volatility could persist in areas such as China property, thus active management remains key.

Asia credit should stay relatively resilient as Asian economies offer a larger growth alpha and lower inflation when compared with developed markets. Price action across Asia credit suggests light positioning and a generally cautious attitude towards the Asia credit market. The reason for caution is not related to the macro conditions or credit fundamentals within Asia but rather the lingering uncertainties on the global macro outlook. Hence clarity on the macro front will help increase conviction amongst Asian credit investors to add risk. Meanwhile, active management remains key as volatility within the China property sector will likely persist in the near term, given overhangs for several weaker players and a gradual economic recovery.

Healthy economic and credit fundamentals help provide downside cushion from market volatilities

Asian economies remain on recovery path helped by the tailwind from China’s reopening while the Asian banking sectors have been relatively more resilient than developed markets. Most Asian central banks are coming to the end of their rate hike cycles, with most of them pausing in their recent monetary policy meetings, as inflation becomes a less pressing issue within Asia, after moving past its peak in 4Q22. This should help to manage duration risk.

Also, the strengthening of local currencies, for example, with Indonesia rupiah appreciating 4.9% year-to-date against U.S. Dollar (USD), while Thailand, India and China appreciating around 0.5-1.5% year-to-date against USD, should help limit imported inflation, allowing central banks to be less hawkish going forward. Looking ahead, with USD being overvalued while the U.S. Federal Reserve is expected to pause soon, we continue to see more upside for Asian currencies and local Asia credit. As USD further weakens, this should allow Asian central banks to devise monetary policy according to local economic and inflation conditions, instead of deploying higher rates just to support their currencies. This should help to limit the downside risks to economic growth due to excessive tightening.

In terms of credit ratings, Asia investment grade (IG) ratings have stabilized in 1Q23 while Asia high yield (HY) saw accelerating downgrades since 4Q21, pointing to a diverging trend. In 2022, Asia has seen about USD20.2bn of IG downgraded, compared to USD7.8bn in 2021. In 2023, there will likely be lower downgrade risk while stable sovereign ratings should help anchor ratings for government related entities, which account for close to 60% of J.P. Morgan Asia Credit Index (JACI).

Within IG, in 2022, Asian IG corporates felt some leverage pressures while interest coverage ratio remains in line with long term average. Fallen angel risks, which result from the possibility and price impact of bond downgrades from IG into HY, are still more idiosyncratic, largely in China property and Macau gaming. In terms of defaults, Asia saw 41 defaults, totaling USD58bn (default rate: 16.5%) in 2022, which included USD43bn bonds from 26 China developers). During 1Q23, Asia saw only one default on USD1.9bn (default rate: 0.7%). As economic activity further picks up, the default rate will likely stay low for the rest of this year, a big improvement from the double-digit default rate in 2022.

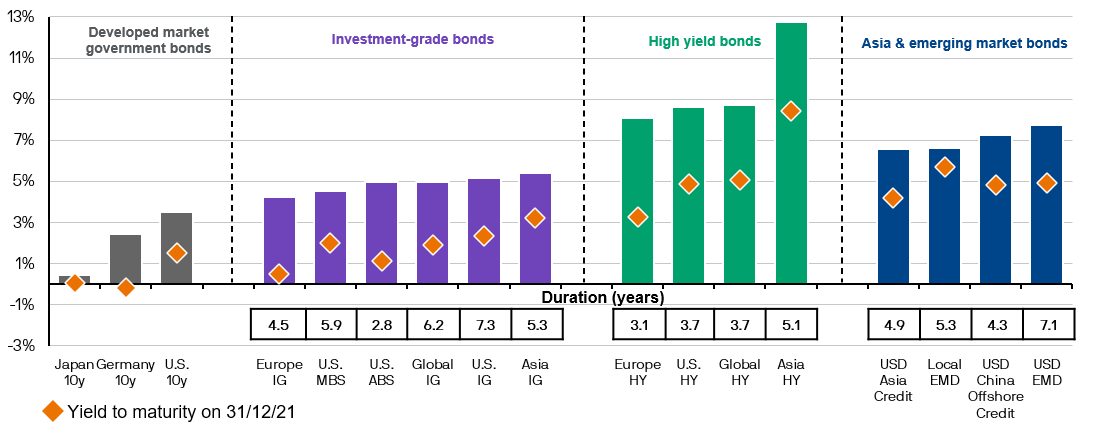

Exhibit 1: Fixed income yields

Yield to maturity

Source: Bloomberg L.P., FactSet, ICE BofA Merrill Lynch, J.P. Morgan Economic Research, J.P. Morgan Asset Management. Based on Bloomberg U.S. Aggregate Credit – Corporate Investment Grade Index (U.S. IG), Bloomberg Euro Aggregate Credit – Corporate (Europe IG), J.P. Morgan Asia Credit Investment Grade Index (Asia IG), Bloomberg Global Aggregate – Corporate (Global IG), Bloomberg U.S. Aggregate Credit – Corporate High Yield Index (U.S. HY), Bloomberg U.S. Aggregate Securitized – Asset Backed Securities (U.S. ABS), Bloomberg U.S. Aggregate Securitized – Mortgage Backed Securities (U.S. MBS), Bloomberg Pan European High Yield (Europe HY), J.P. Morgan Asia Credit High Yield Index (Asia HY), ICE BofA Global High Yield (Global HY), J.P. Morgan GBI-EM Global Diversified (Local EMD), J.P. Morgan EMBI Global (USD EMD), J.P. Morgan Asia Credit Index (JACI) (USD Asia Credit), J.P. Morgan Asia Credit China Index (USD China Offshore Credit). Duration is a measure of the sensitivity of the price (the value of the principal) of a fixed income investment to a change in interest rates and is expressed as number of years. Spread durations are shown for Asia IG, Asia HY, USD EMD, USD Asia Credit and USD China Offshore Credit. Rising interest rates mean falling bond prices, while declining interest rates mean rising bond prices. Yields are not guaranteed, positive yield does not imply positive return. Past performance is not a reliable indicator of current and future results. Guide to the Markets – Asia. Data reflect most recently available as of 28/04/23.

Investment implications

As market volatility will likely stay elevated in the near term, similar to equities, we prefer to stay defensive within Asia credit. With yields higher across Asia, investors do not have to go to HY to pick up decent income and we continue to see pockets of opportunities within the IG space, as illustrated by Exhibit 1. Relative to IG peers in U.S. and emerging markets, Asia credit valuations look reasonable, while offering attractive carry at the same time.

Admittedly, active management remains key given investors’ ongoing concerns with regards to the China property sector. In our view, the China housing market is still at an early stage of recovery and it could take some time before sector fundamentals stabilize. Hence, further credit differentiation with more defaults are likely, highlighting the need to remain up in quality.