Finding value in passive hedging

05/13/2020

In Brief

- The increased level of interest rate volatility in the currency swap1 market has received considerable attention from market participants, as we described in the April 2020 Currency Thought, “Tracking Funding Stress in Currency Markets.”

- We commented on the recent strain in USD funding markets and the subsequent spillover to the pricing of currency swaps, which is leading to considerable distortions in market pricing.

- In this piece, we concentrate on the implications of these stresses for hedging USD currency exposure using traditional methods of implementation.

- Furthermore, we will demonstrate how using active tenor management has resulted in improved hedging outcomes, especially in the recent period of sharply falling US interest rates alongside considerable volatility in the cross-currency basis.

Passive hedging performance

Passive currency hedges can be implemented using currency forwards based on a regular fixed roll cycle. The most popular method is to use a one-month benchmark hedge2, but in some cases a passive currency hedge can be implemented using an overlapping laddered approach3. There may be other types of implementation but we focus specifically on the performance of the one-month benchmark hedge and the six- month overlapping laddered hedge.

The primary driver of any excess return is the mismatch between the duration in the portfolio’s hedges and the benchmark hedge. The overlapping hedge would be expected to generate positive excess returns if the interest rate differentials4 of the portfolio are realised to be better than the benchmark hedge.

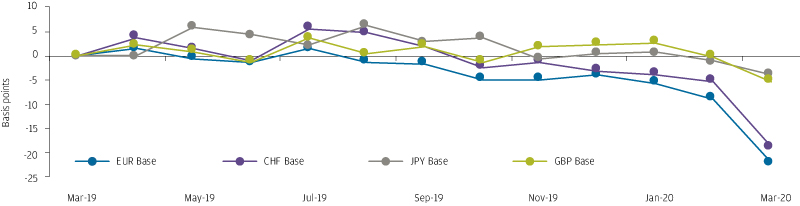

We consider the performance over the 12-month period from 31 March 2019, which exhibited a sharp decrease in US borrowing costs and, more lately, a dramatic increase in USD funding stress. Exhibit 1 shows how the overlapping hedge has underperformed relative to the benchmark hedge.

EXHIBIT 1: THE CUMULATIVE EXCESS RETURN OF THE OVERLAPPING HEDGE RELATIVE TO THE BENCHMARK HEDGE FOR HEDGING USD FOREIGN CURRENCY EXPOSURE

Source: J.P. Morgan Asset Management, Bloomberg; data as of 31 March 2020.

Past performance is not a reliable indicator of current and future results.

Despite the positive start, the performance of the overlapping hedge has broadly underperformed the benchmark hedge in all base currencies over the period. This underperformance was driven by the overlapping hedge’s shorter US interest rate position compared to the benchmark in a period when the Federal Reserve (the Fed) cut interest rates sharply. As US interest rates fell faster, the overlapping hedge underperformed the benchmark as it has locked in USD borrowing levels at higher levels for a longer period.

Enhancing passive hedging returns

The introduction of flexibility in the duration selection of currency hedges can add value against the benchmark hedge. The ability to move the duration of the currency hedges between the benchmark hedge and longer-dated overlapping portfolios while maintaining low transaction costs can yield positive excess returns.

In simple terms, we seek to have shorter-dated contracts when we believe US interest rates will fall faster than forward prices or if we believe the cross-currency basis will tighten to better levels in the future. In contrast, we seek to use longer-dated overlapping hedges when we anticipate higher US interest rates or more adverse levels in the cross-currency basis.

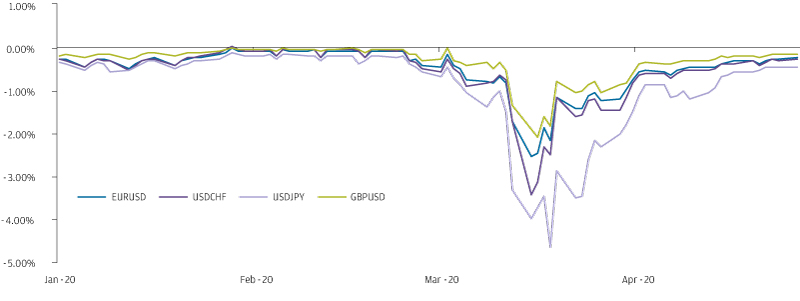

The risks and challenges have been significant for hedging USD exposure for passive hedgers this year. The combination of the Fed cutting rates by 150 basis points in less than three weeks, the rapid deterioration of US funding markets and subsequent widening in the cross-currency basis (see Exhibit 2), and the significant drop in swap market liquidity made rolling USD hedges exceptionally challenging.

Our investment process seeks to capture these opportunities, which we successfully implemented by changing the tenor of the hedges in portfolios for clients who allow such flexibility. As concerns over the economic impact from coronavirus started to emerge, we were mindful of an aggressive response from the Fed. As a result, we shortened the duration of the USD hedges in portfolios by the end of February 2020.

This view was subsequently realised; however, the rapid reduction in US policy rates coincided with a rapid widening in cross-currency basis, which meant that not all gains accrued to the portfolio instantly. We maintained short-dated contracts over this period with the view that the Fed would inject USD liquidity, which would reduce the cross-currency basis. This view was also subsequently realised.

We therefore successfully avoided locking in adverse funding levels in portfolios. The enhanced flexibility allowed our client portfolios to outperform both the overlapping and the benchmark hedge over the 12-month period.

EXHIBIT 2: CURRENCY BASIS – ONE MONTH VS. OVERNIGHT INDEXED SWAP (OIS)

Source: J.P. Morgan Asset Management, Bloomberg; data as of 31 March 2020.

Strategy considerations

The Fed has introduced a range of large liquidity measures to improve the functioning of money markets and increase the availability of US dollars. Specifically, the re-activation of the Fed’s central bank FX swap facility has increased the cross-border availability of US dollars. The market impact from these measures has been rapid, as illustrated by the normalisation in cross currency basis over the last few weeks.

We believe these supportive measures, along with improving financial intermediation, may deliver further normalisation of the cross-currency basis, which may provide a good opportunity to move to longer-dated hedges

Furthermore, we recognise the benefits of overlapping hedges (such as lower overall hedge transaction costs and a smoother cash-flow profile) also reduce the implicit transactions costs associated with rebalancing the underlying asset portfolio. For that reason, we are aiming to move to longer-dated contracts using the overlapping structure for client portfolios as the next important step for hedging USD currency exposures.

1 The currency swap instrument in this document is considered as the combination of a foreign exchange (FX) spot contract combined with an equal and offsetting FX forward contract.

2 The one-month benchmark hedge is a popular performance metric for evaluating excess returns due to its adoption by well-known hedged benchmark indices.

3 The overlapping laddered approach is where the notional size of the hedge is split across equally-weighted tranches, with each tranche staggered monthly. For example, a six-month overlapping hedge restructure would use six currency forwards, each 1/6th of the total exposure and maturities staggered

4 The interest rate differentials (or carry costs) can be improved if the portfolio can realise lower implied US risk free rates, higher domestic risk-free interest rates and better levels of cross currency basis (which is typically negative for hedging USD exposure) implied in currency forward contracts.

5 Due to the asymmetric nature of the 1-month benchmark, we assume the portfolio can range from being neutral or have longer dated contracts (as in the overlapping hedge) relative to the benchmark.

Opinions, estimates, forecasts, projections and statements of financial market trends are based on market conditions at the date of the publication, constitute our judgment and are subject to change without notice. There is no guarantee they will be met. Provided for information only, not to be construed as investment recommendation or advice.

0903c02a828afbc0