Credit Spreads Reflect Strong Risk Appetite

Credit spreads, which measure the extra yield investors require for taking on credit risk above government bonds, have been tightening across the APAC region in the past year until conflicts in Middle East escalate. This trend signals that global and regional investors are more comfortable with Asia credit risk and willing to accept lower compensation for it. The narrowing of spreads is not just a technical phenomenon—it reflects a broader risk appetite and confidence in the region’s strong credit fundamentals.

A healthy regional macroeconomic backdrop is a key driver of this trend. Robust GDP growth in the U.S. and resilient exports from China, has fostered a positive environment for credit. Asia’s technology sector, has also benefited from the surge in AI-related investments. This influx of capital has supported growth and reinforced the region’s economic outlook, encouraging investors to take on more credit risks. However, global geopolitical risk is still a major risk to watch.

Market Resilience and Supply Dynamics

While the overall macroeconomic outlook remains positive, evolving geopolitical risks continue to influence credit market behavior. With inflation trends and central bank policies becoming more uncertain, investors are increasingly favoring shorter maturities, which have proven more resilient than longer-term bonds. The sell-off in longer-dated credit reflects caution amid global uncertainties, while the short end remains stable—a trend consistent with liquidity-focused investment strategies.

Supply dynamics can also cause temporary disruptions. Recent large deals from U.S. tech giants have attracted significant attention and added substantial supply to the market. Meanwhile, local currency issuance has quietly increased in recent years, as issuers prefer lower regional interest rates and investors seek diversification away from the USD market. So far, the market has absorbed this supply well, but significant new issuance can temporarily affect spreads, market stability, and risk premiums. Investors should remain vigilant.

Financial Institutions: Strength and Stability

Asia’s financial institutions continue to demonstrate solid fundamentals. Exposure to private credit among Asian banks and insurers is notably lower than in Western markets. This conservative approach, rooted in historical and structural factors, has contributed to the region’s financial stability. Funding conditions for Asian financial institutions remain comfortable, supporting their ability to withstand shocks and maintain healthy balance sheets.

Regulatory developments are further strengthening the sector. The implementation of global standards such as Basel IV and Enhanced Solvency Requirements for insurers are designed to improve the resilience of financial institutions, especially during periods of crisis. These regulations encourage banks and insurers to issue more capital securities, such as Tier 2 and AT1 bonds, to meet stricter capitalization requirements. While these changes may alter credit behavior and supply dynamics, they ultimately contribute to a more robust financial system.

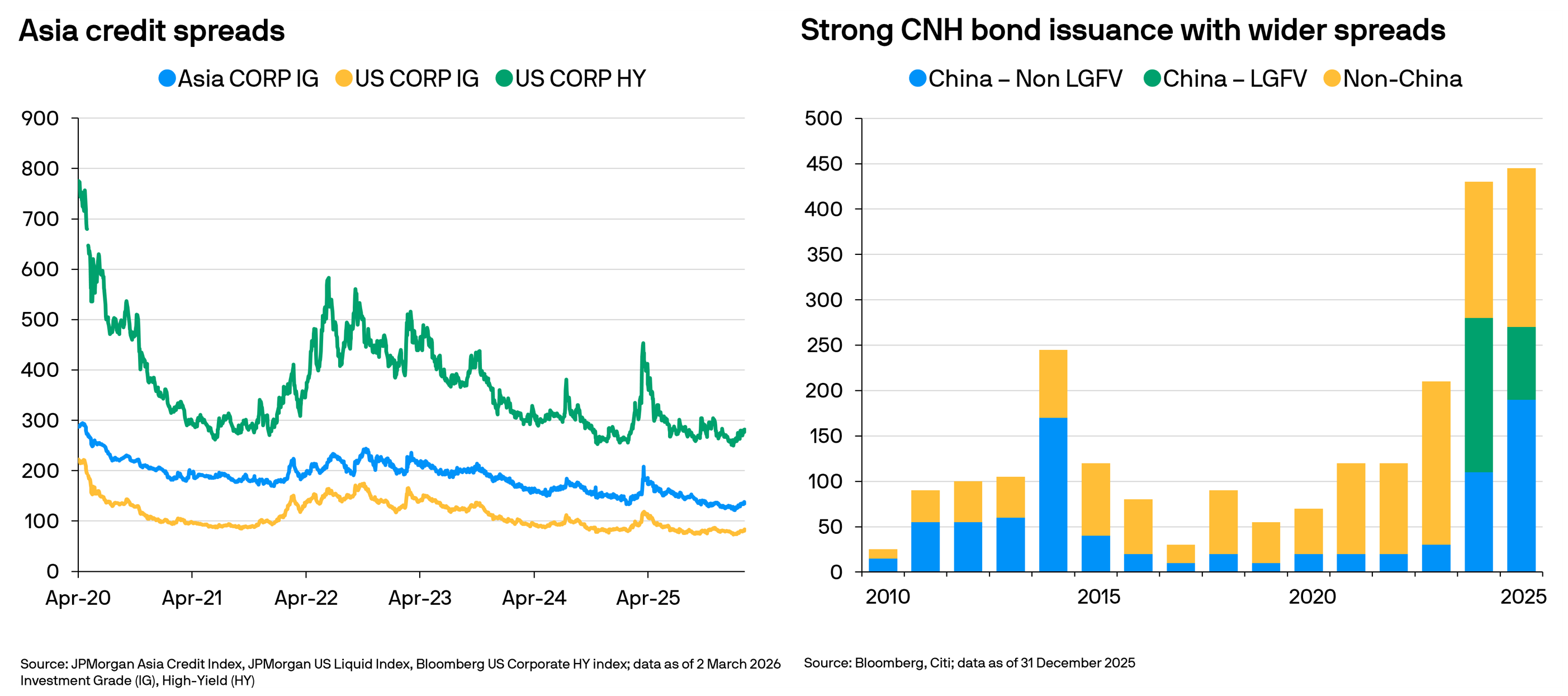

Dollarization, CNH Bond Issuance, and Local Market Opportunities

A notable trend in Asia’s credit markets is the shift away from exclusive reliance on U.S. dollar bonds. Major Chinese internet companies previously issued only USD bonds due to their corporate structures and currency needs. However, in the past one to two years, these companies have increasingly allocated a significant portion—at least one third—of their bond issuance to CNH (offshore RMB) bonds. This move reflects a growing preference for diversification and the advantages of funding in local currencies.

For issuers, CNH bonds present relatively attractive funding costs and flexibility. For investors, local markets—including CNH—often provide wider credit spreads compared to equivalent USD bonds, helping to meet yield expectations while benefiting from lower volatility. Local markets also tend to be more insulated from global shocks, offering a valuable balance in diversified portfolios. The booming issuance in CNH and other local currencies underscores Asia’s evolving market structure and the region’s move toward a more multipolar funding environment.

Conclusion: Solid Fundamentals, Tighter Valuations

In summary, Asia’s credit markets in 2026 remain supported by healthy fundamentals, greater diversification of bond issuance currencies and solid investor demand. Investors are increasingly comfortable with regional credit risks, driving tighter valuations, while technical factors remain supportive, while geopolitical risk is the downside risk to rock the boat.

The shift toward local bond issuance is creating new opportunities for diversification and helping investors to balance portfolios amid global volatility. While supply dynamics, geopolitical risks, and regulatory changes warrant ongoing attention, the region’s credit landscape remains fundamentally solid. As the market evolves, a cautious yet optimistic approach will help investors navigate the challenges and capitalize on Asia’s enduring strengths.