Implications of Middle East tensions for the global economy and markets

We explore the potential economic and market scenarios stemming from escalating tensions in the Middle East.

Read more

ETF Perspectives

Explore insights from J.P. Morgan Asset Management’s ETF research. In addition discover data and commentary on current topics related to ETF classes and strategies.

Sustainable Investing Insights

We believe that ESG considerations can play a critical role in a long-term investment strategy.

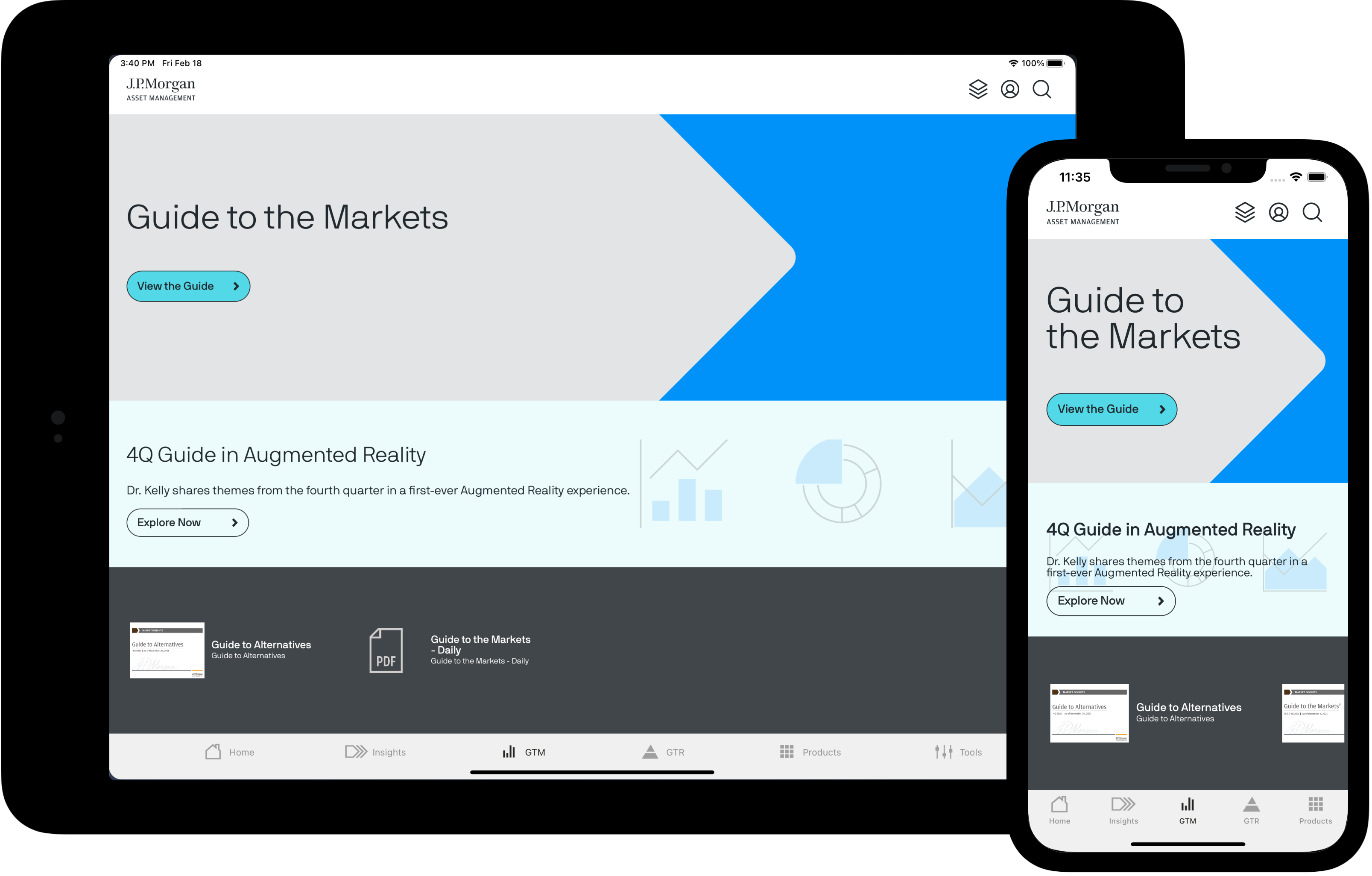

24/7 access to market views, allocation insights, portfolio analytics, presentation tools and more