Investing in forestry: The case for timber allocations in pension portfolios

Ben Payet

23/05/2022

How can pension schemes achieve effective inflation protection, maintain a low volatility return profile while also benefiting from regular income, and attractive sustainability characteristics?

For defined benefit pension schemes with long-term investment horizons, the answer could be provided by investing in forestry, via a portfolio allocation to timber assets.

A timber allocation provides several benefits

Attractive risk and return profile

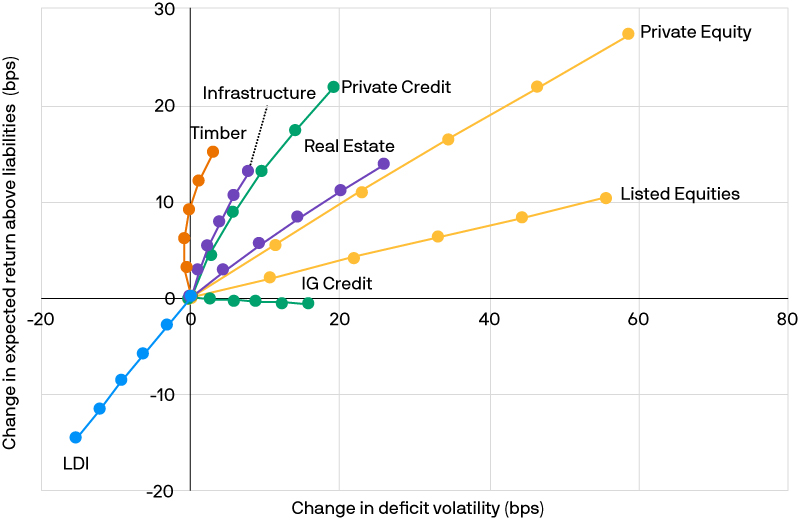

Our risk/return analysis, based on the typical asset allocation of a large UK defined benefit scheme, suggests that a small allocation to timberland (up to 5%) funded from existing allocations could improve portfolio efficiency with improved expected returns for the same level of portfolio volatility relative to pension liabilities.

Exhibit 1 : Risk/return impact of reallocating 1%-5% of current portfolio allocations to selected asset classes

Change in surplus risk and return

Source: J.P. Morgan analysis1. For illustrative purposes only.

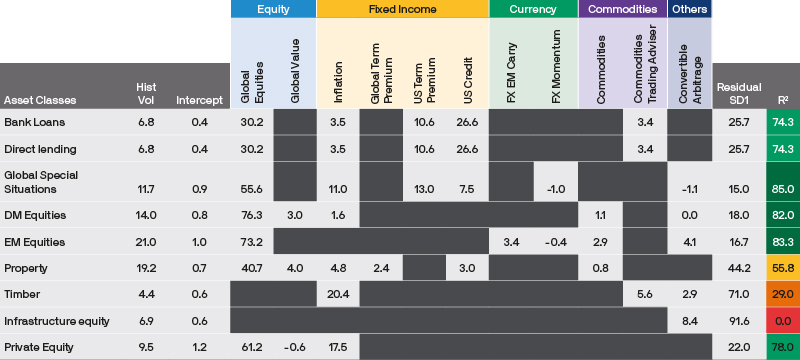

Low correlation to other assets

Timber can bring strong diversification properties to portfolios. In our regression based factor model, timber, along with infrastructure equity, has a low R-squared figures, which mean historical returns are not well explained by most standard investment factors. In turn, this means that these asset classes arguably bring new factor exposures to a portfolio.

Exhibit 2 : Asset class correlations to standard investment factors

Source: J.P. Morgan Asset Management. For illustrative purposes only. Past performance is not indicative of future results. Factor loadings/estimates are based on return data for the 18 year, 10 month period from January 2003 to November 2021.Analysis conducted on GBP hedged asset classes.

Defensive exposure in volatile markets

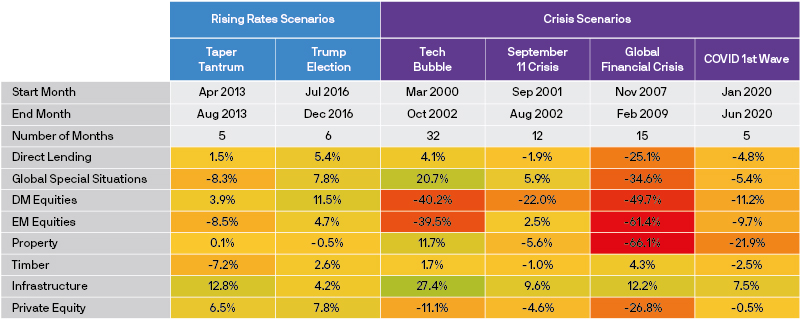

In historical market stress events, exposure to diversifying risk factors not found in public markets has helped forestry to perform well compared to the majority of risk assets, with only modest losses (or even modest gains) produced through the biggest crises and rising rate scenarios of the last 20 years.

Exhibit 3 : Historical asset class stress test

Source: J.P. Morgan Asset Management. For illustrative purposes only. Past performance is not indicative of future results.

Source: J.P. Morgan Asset Management. For illustrative purposes only. Past performance is not indicative of future results.

Inflation protection

Forestry exhibits a strong positive correlation to inflation, which is helpful in the current inflationary economic environment.

Exhibit 4 : Correlations between asset classes and inflation.

Source: J.P. Morgan Asset Management Guide to Alternatives 2021.

Source: J.P. Morgan Asset Management Guide to Alternatives 2021.

Alignment with sustainability goals

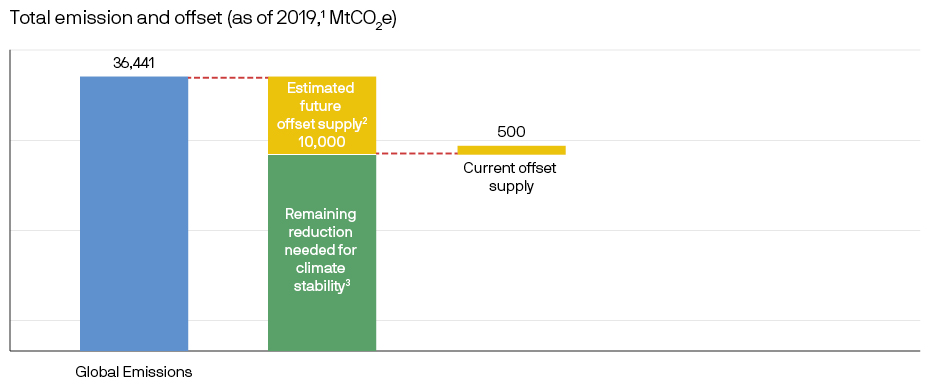

Investing in the preservation of forest land results in environmental and societal benefits, which align with many clients’ corporate values. Forestry, for example, provides an effective and scalable mechanism for sequestering atmospheric carbon, and represents around 40% of the current supply of carbon offsets at a time when many businesses are looking to achieve low or even net-zero carbon emissions from their operations.

Exhibit 5 : Global carbon emissions and offsets Source: Global Carbon Atlas (http://www.globalcarbonatlas.org/en/CO2-emissions); Carbon Registries (total of carbon offset registered on Climate Action Reserve, American Carbon Registry, Carbon Plan, Gold Standard, Verra, Clean Development Mechanism); ARB is not included since projects are also registered in American Carbon Registry, Climate Action Reserve, and Verra. 1 Data as of 2019 - unless unavailable (Carbon Plan as of 2021 and Verra as of latest yearly data). 2 Annual carbon reduction needed to achieve the Paris Agreement goal of 1.5oC temperature reduction by 2100.

Source: Global Carbon Atlas (http://www.globalcarbonatlas.org/en/CO2-emissions); Carbon Registries (total of carbon offset registered on Climate Action Reserve, American Carbon Registry, Carbon Plan, Gold Standard, Verra, Clean Development Mechanism); ARB is not included since projects are also registered in American Carbon Registry, Climate Action Reserve, and Verra. 1 Data as of 2019 - unless unavailable (Carbon Plan as of 2021 and Verra as of latest yearly data). 2 Annual carbon reduction needed to achieve the Paris Agreement goal of 1.5oC temperature reduction by 2100.

The strategic case for timber investing

Timber provides a middle ground between the return potential of liquid alternatives and the income provided by illiquid core real assets, while timber’s ability to offset greenhouse gas emissions through the sequestration of atmospheric carbon provides additional sustainability credentials to any portfolio allocation.

At J.P. Morgan Asset Management, our sustainable timberland investor and forestry management company Campbell Global offers expert timber investment solutions.

1 The analysis is relative to typical Defined Benefit (DB) pension plan liabilities in the United Kingdom. Please contact your local J.P. Morgan representative for bespoke analysis.

09s8221605122103