As volatility continues to challenge markets, investors are looking further afield to generate returns, both geographically and beyond traditional balanced portfolios. As a result, liquid alternatives are becoming increasingly popular in the search for enhanced returns and portfolio diversification1.

Beyond returns, investors are also looking for investment solutions that reflect not only their financial goals but also their values.

We share how we employ our tried and tested macro process, sustainably, to help investors align their return goals with their values2.

The big picture

The war in Ukraine has further challenged risk assets in 2022 by triggering a commodity shock, which put further upward pressure on inflation. Inflation was already persistently high due to labour market strength and COVID-19-related supply chain issues, and has seen central banks turn increasingly hawkish this year, with a sharp re-pricing of interest rate expectations.

Central banks are now explicitly aiming to slow economic activity to reduce demand-side inflation pressures. This adds to the underlying slowing we were already tracking in our cyclical framework at the turn of the year and we estimate the chances of central banks engineering a ‘soft-landing’ where economic activity does not dip substantially below trend as low.

In recent weeks, strict COVID-19 control policies in China in response to an Omicron wave have hit activity markedly. Supply chain bottlenecks stemming from this may result in further inflationary pressures.

Against this backdrop, it is understandable for investors to focus on volatility management in the near term. Still, heightened market volatility has given rise to a shifting array of price dislocations and unexpected opportunities2.

Big trends drive opportunities

We believe that the cyclical macro economic backdrop, as well as long-term structural changes shaping the world, are significant drivers of asset prices. Organising these changes into a set of macro themes3 provides a framework to focus our research efforts in areas that we believe will have the most impact and offer attractive investment opportunities. Our themes are categorised as either secular (long term) or cyclical (medium to shorter term).

3. Source: J.P. Morgan Asset Management, as at 30.04.2022. US theme includes Canada. Opinions, estimates, forecasts, projections and statements of financial market trends are based on market conditions at the date of the publication, constitute our judgment and are subject to change without notice. There can be no guarantee they will be met.

3. Source: J.P. Morgan Asset Management, as at 30.04.2022. US theme includes Canada. Opinions, estimates, forecasts, projections and statements of financial market trends are based on market conditions at the date of the publication, constitute our judgment and are subject to change without notice. There can be no guarantee they will be met.

As illustrated above, we see the US, Asia Pacific ex-China and emerging markets as being a cyclical slowdown, driven by weaker growth, sentiment and liquidity. Meanwhile, Europe and China are in contraction due, respectively, to the commodity price shock and negative impact on confidence, and renewed COVID-19 restrictions.

3. Source: J.P. Morgan Asset Management, as at 30.04.2022. US theme includes Canada. Opinions, estimates, forecasts, projections and statements of financial market trends are based on market conditions at the date of the publication, constitute our judgment and are subject to change without notice. There can be no guarantee they will be met.

3. Source: J.P. Morgan Asset Management, as at 30.04.2022. US theme includes Canada. Opinions, estimates, forecasts, projections and statements of financial market trends are based on market conditions at the date of the publication, constitute our judgment and are subject to change without notice. There can be no guarantee they will be met.

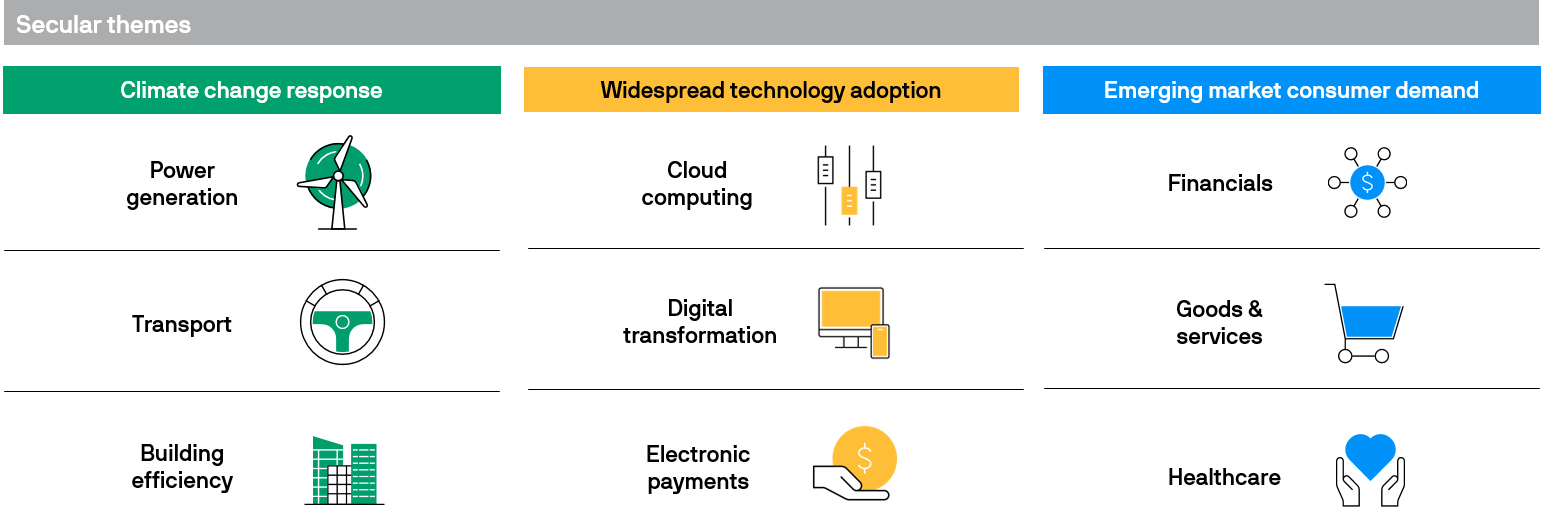

When it comes to secular themes, climate change response reflects the increased focus on sustainability from governments, companies and individuals, which presents multi-year opportunities across industries, such as power generation and construction, as efforts are made to transition to a lower carbon economy.

The widespread adoption of new technologies is another secular theme, in which our main focus is in cloud computing. We see a significant and underpriced shift in enterprise workloads moving from on-premises to cloud infrastructures, which supports the investment thesis for cloud computing providers1.

Another secular theme relates to consumer demand in emerging markets, where we are seeing the growth of the middle class leading to rising demand for financial services, and we hold select Indian banks which are high quality and well-placed to benefit from rising financial penetration in the market1.