JPMorgan Asia Growth and Income (JAGI) aims to provide investors with both capital growth and income by investing in some of the best ideas across Asia (ex-Japan).

The Company differs from its peers as its managers adopt dual perspectives to identify the region’s most compelling investment opportunities. They consider the ‘big picture’ – the economic performance of various countries within the Asian region, and the outlook for particular industries. But they pay equal attention to the detailed fundamentals of individual companies, and target only quality companies with competitive advantages, strong profitability, low debt, and a capacity to grow and generate positive returns over many years. These differing perspectives, supported by JPMorgan’s deep, on-the -ground research resources, provide the managers with additional insights and ideas relative to other managers focused solely on individual (‘bottom-up’) stock picking.

Digitalisation and the growth of Asia’s middle classes predicted to drive future investment performance

The growth prospects of the companies JAGI owns are often supported by long-term structural trends such as digitalisation and the rise of Asia’s middle classes. As elsewhere, digital technologies are permeating all spheres of daily life across the region and disrupting traditional, often inefficient industries. Some of the largest companies in the region are focused on e-commerce, internet content, video steaming and gaming, while the convenience of online banking and payment systems is driving the expansion of companies offering these services. In the commercial world, factory automation and robotics, data processing and the digitalisation of administrative processes are increasing productivity and profits. Many of JAGI’s holdings, such as China’s internet content giant Tencent, online retailer Meituan, Taiwan Semiconductor Manufacturing Company, and IT services provider Infosys are at the cutting edge of the digitalisation trend. The portfolio also has exposure to the myriad opportunities created by Asia’s burgeoning middle classes. Incomes are rising across the region, and this is generating demand for a wide variety of consumer goods and services, including cars, dining out, tourism, banking, insurance and healthcare. Holdings such as Samsung Electronics, Maruti Suzuki, restaurant chain Yum China, travel website Trip.com, and pan-Asian insurer AIA are all set to benefit from rising household incomes and aspirational spending.

A contrarian view on China

Proactive, high conviction investment management is another of JAGI’s defining characteristics. Its managers are not afraid to hold strong views on particular countries, sectors, or stocks, and to back their convictions by taking bigger or smaller positions relative to the benchmark, sometimes in defiance of general market consensus. Their view on China is one notable example of this active management approach. While most investors are presently bemoaning the ‘sluggishness’ of China’s post-pandemic recovery, and worrying about China’s property market, JAGI’s managers are optimistic about the country’s medium-term growth prospects. They argue that although China is set to grow more slowly than before the pandemic, forecast growth of around 5% this calendar year and next is still very strong in absolute terms and relative to the insipid growth projections of the major western economies.

This upbeat assessment is reflected in the stocks held in the portfolio – exposure to China and Hong Kong is one of the Company’s largest overweights, manifest via above benchmark positions in companies such as Tencent, and AIA, mentioned above, and Hong Kong Exchanges and Clearing. And the managers are looking to gain greater exposure to China’s recovery, especially in sectors benefiting from rising demand for outbound tourism. They have made recent investments in Thai airports, and hospitals set to benefit from medical tourism.

Further examples of the managers’ proactive management style include above benchmark positions to Indonesia’s well-run banks, and to Korean tech stocks, and significantly below benchmark exposures to Taiwan and India, markets the managers view as excessively expensive.

Quality is a key focus

JAGI’s focus on high quality companies, with robust balance sheets and strong growth prospects, means that while, on average, holdings tend to be more expensive than the market, their debt levels are much lower than the market average - an especially reassuring characteristic in the current, rising rate environment. For the managers, the calibre of a business’s management team and governance are additional, essential measures of its quality. They favour companies with clear, well-executed business strategies, transparent governance practices and a willingness to return excess cash to shareholders in the form of higher dividends and share buybacks.

Performing through recent bumpy times

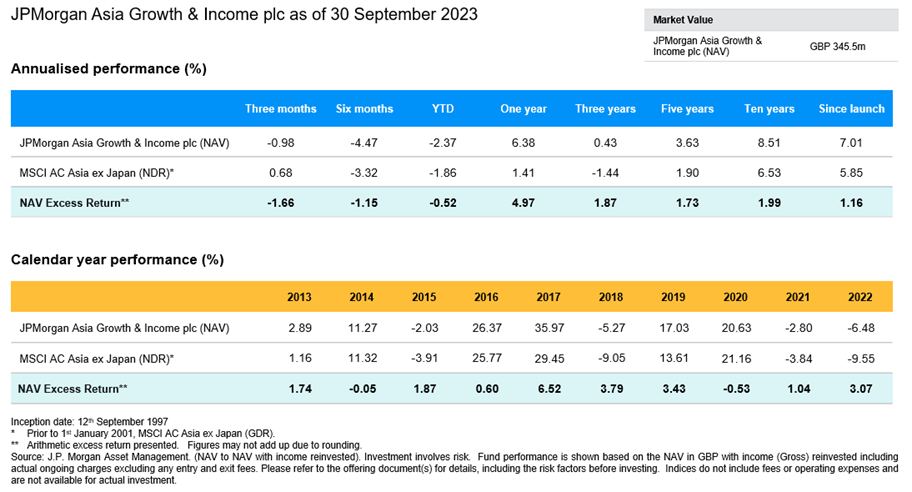

The effectiveness of the managers’ proactive, high conviction approach and their focus on growth and quality can be measured by the Company’s long-term outperformance. It has generated an average annual return of 8.5% per year on an NAV basis, over the ten years to end September 2023, decisively above the average annual benchmark return of 6.5% over the same period. And this performance has been consistent over time – JAGI has managed outperformed the benchmark throughout a variety of market conditions encompassing wide fluctuations in market returns and a variety of challenges including a global pandemic, war in Eastern Europe, geo-political tensions between China and the west and aggressive interest rate increases. This should offer shareholders some confidence in the trusts ability to navigate market fluctuations, while providing regular income, in the year ahead.

More Insights

Image source: Getty

Source: J.P. Morgan Asset Management. Performance data has been calculated on a NAV to NAV basis, including ongoing charges and any applicable fees, with any income reinvested, in GBP. The performance of the company's portfolio, or NAV performance, is not the same as share price performance and shareholders may not realise returns which are the same as NAV performance. Past performance is not a reliable indicator of current or future results.

Summary Risk Indicator

The risk indicator assumes you keep the product for 5 year(s). The risk of the product may be significantly higher if held for less than the recommended holding period

Investment Objective:

Aims to provide capital growth from a diversified portfolio of around 50 to 80 companies quoted on the Asian stock markets, excluding Japan. The Company pays quarterly dividends equivalent to 1% of its net asset value, set on the last business day of each financial quarter. The Company also has the ability to use gearing up to a maximum level of 20% of net assets to increase potential returns to shareholders.

Risk profile:

- Exchange rate changes may cause the value of underlying overseas investments to go down as well as up.

- Investments in emerging markets may involve a higher element of risk due to political and economic instability and underdeveloped markets and systems. Shares may also be traded less frequently than those on established markets. This means that there may be difficulty in both buying and selling shares and individual share prices may be subject to short-term price fluctuations.

- External factors may cause an entire asset class to decline in value. Prices and values of all shares or all bonds and income could decline at the same time, or fluctuate in response to the performance of individual companies and general market conditions.

- This Company may utilise gearing (borrowing) which will exaggerate market movements both up and down.

- This Company may also invest in smaller companies which may increase its risk profile.

- The share price may trade at a discount to the Net Asset Value of the Company.

- The Company may invest in China A-Shares through the Shanghai-Hong Kong Stock Connect program which is subject to regulatory change, quota limitations and also operational constraints which may result in increased counterparty risk.

This is a marketing communication and as such the views contained herein do not form part of an offer, nor are they to be taken as advice or a recommendation, to buy or sell any investment or interest thereto. Reliance upon information in this material is at the sole discretion of the reader. Any research in this document has been obtained and may have been acted upon by J.P. Morgan Asset Management for its own purpose. The results of such research are being made available as additional information and do not necessarily reflect the views of J.P. Morgan Asset Management. Any forecasts, figures, opinions, statements of financial market trends or investment techniques and strategies expressed are unless otherwise stated, J.P. Morgan Asset Management’s own at the date of this document. They are considered to be reliable at the time of writing, may not necessarily be all inclusive and are not guaranteed as to accuracy. They may be subject to change without reference or notification to you. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested. Changes in exchange rates may have an adverse effect on the value, price or income of the products or underlying overseas investments. Past performance and yield are not reliable indicators of current and future results. There is no guarantee that any forecast made will come to pass. Furthermore, whilst it is the intention to achieve the investment objective of the investment products, there can be no assurance that those objectives will be met. J.P. Morgan Asset Management is the brand name for the asset management business of JPMorgan Chase & Co. and its affiliates worldwide. To the extent permitted by applicable law, we may record telephone calls and monitor electronic communications to comply with our legal and regulatory obligations and internal policies. Personal data will be collected, stored and processed by J.P. Morgan Asset Management in accordance with our EMEA Privacy Policy www.jpmorgan.com/emea-privacy-policy. Investment is subject to documentation. The Annual Reports and Financial Statements, AIFMD art. 23 Investor Disclosure Document and PRIIPs Key Information Document can be obtained free of charge in English from JPMorgan Funds Limited or at www.jpmam.co.uk/investmenttrust. This communication is issued by JPMorgan Asset Management (UK) Limited, which is authorised and regulated in the UK by the Financial Conduct Authority. Registered in England No: 01161446. Registered address: 25 Bank Street, Canary Wharf, London E14 5JP.

09nd231511165206